The Quarterly Focus – Q2 2026

The More Things Change …

Global stock markets surged over the last three months. Despite periodic pullbacks related to shifting Federal Reserve rate hike expectations and the war in Iran, strength in the technology and materials sectors lifted equities across North America and much of Asia. Following a sharp 9% selloff during the month of March, the S&P 500 Index climbed ~17% , an explosive run driven by resilient corporate earnings, artificial intelligence (AI) related investment and rising semiconductor and memory stocks. Meanwhile, Canada’s S&P/TSX Composite Index gained ~7%, supported by bank outperformance and rising commodity prices. It has been one of the strongest stock market rallies in recent memory.

As a rule, we try to strike a balanced tone in these letters. Financial media is often hyperbolic—on any given day the sky is either falling or something is being revolutionized—and we default to dialing down the drama. In this instance, however, there is something to be much ado about.

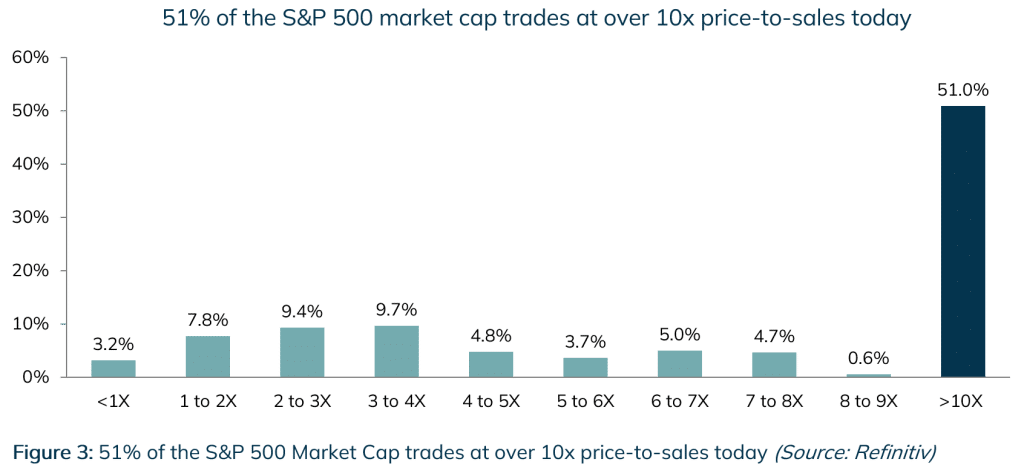

From where we sit, the world is living through both a technological revolution and another hype cycle. The largest capital expenditure (CapEx) cycle in history is underway, centered on a technology (AI) that promises to change not only the nature of work but perhaps even human cognition. At the same time, valuations for many publicly traded stocks have moved into what would be considered extremely expensive territory under all but the most optimistic outcomes. Suffice to say, an S&P 500 Index where roughly half the constituents trade at 10x Price-to-Sales is frothy. A stock market that absorbs massive IPOs, with little or no earnings, without any apparent indigestion, is manic.

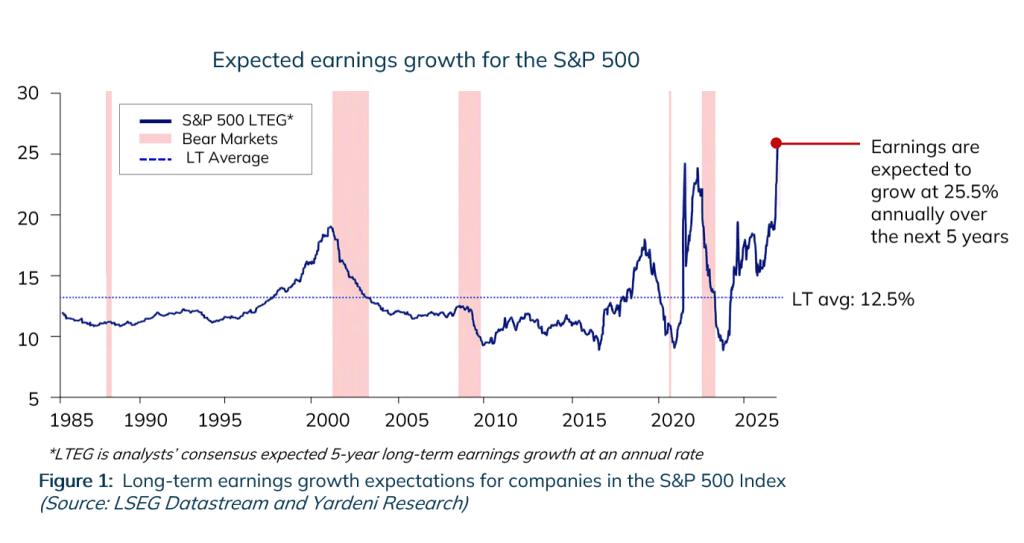

Figure 1.0, which highlights long-term earnings growth expectations for companies in the S&P 500 Index, shows just how extreme assumptions have become. 25.5% long-term earnings growth is reflecting extremely high expectations.

We would note that growth expectations are now double their long-term average (and stock market declines have tended to follow previous peaks).

In short, nearly every traditional indicator of late-stage market exuberance is flashing red. Yet many investors appear to find current conditions unremarkable, and defend these valuations as warranted. This, too, is a reliable signal.

While we generally argue clients are better off ignoring the news, there are two instances in which we deviate from this stance and suggest paying attention. The first is when investors are panicked, asset prices are collapsing, and fear has produced excessively pessimistic assumptions about the future. In these moments—such as 2002, 2009, and 2020—those with strong stomachs can often capitalize on exceptional long-term buying opportunities.

The second is when investors have become so complacent that they have abandoned any meaningful notion of risk. When people genuinely believe stock prices can only rise, those with common sense question their sanity, and everyone surrounding us appears to profit from abandoning principle, this is when the greatest investment risk exists. And it is time to proceed with caution.

We believe we are in the second moment.

A tale of two economic realities (future promise versus impossible maths)

In 1974, physicist Richard P. Feynman wrote that, “The first principle is that you must not fool yourself—and you are the easiest person to fool.” To follow in this spirit of not fooling ourselves, we will take a little more time this quarter to establish some facts on the ground. We hope the abnormality of this period will then become self-evident.

To begin: economic reality today presents as two different worlds. There is the economy directly touched by artificial intelligence, semiconductor investment and hyperscale data center construction, and there is the rest.

In America, the tale of two economic realities is most apparent. The United States is among the clearest beneficiaries of the AI capital expenditure cycle in the world. American investment in data centers, advanced semiconductors, electrical infrastructure, cloud computing and power generation is currently occurring at a pace rarely seen outside of wartime mobilizations or major industrial revolutions.

Yet outside of AI-sensitive industries, much of the American economy has expanded only modestly, if at all. In fact, as much as three-quarters of U.S. economic growth during the first quarter of 2026 was directly or indirectly attributable to AI-related capital spending. Many areas of the U.S. would otherwise be considered in recession.

In Canada, where there is no large domestic semiconductor industry or meaningful hyperscale infrastructure buildout, growth has been much more modest. Canadian economic growth has been constrained by slower consumer spending and a continuing adjustment to U.S. tariff policies. The only real bright spots have been from the accidental beneficiaries of the war in Iran. Higher commodity prices have boosted commodity producers, financial institutions and resource-oriented businesses.

Meanwhile, the interest rate environment has shifted meaningfully. As this letter goes to print, the U.S. has signed a memorandum of understanding with Iran that has soothed investor apprehension (even if it expires in 60 days). Oil prices have fallen meaningfully from wartime highs, and shipping through the Strait of Hormuz has been slowly increasing.

Unfortunately, much economic damage has already been done. Headline inflation came in at 3.2% in May for Canada, and 4.2% in the same period for the U.S. Where rate cuts were previously on the table at the Federal Reserve, such discussions have all but disappeared.

Moreover, there may yet be delayed impacts from earlier fighting. Inventory levels for many important input goods have been depleted. We may still feel some impact on supply chains later in the year. Peace is also by no means secure.

In short, economic growth in North America has been robust where there has been exposure to the massive AI CapEx cycle, and anemic elsewhere. The monetary outlook has tightened. This is not a supportive backdrop for equities.

Though one would never know it looking at the stock market.

Future Promise …

This brings us to the stock market, in which, as we’ve already established, many indicators of late-stage exuberance are flashing red.

Before we go there, however, we should first examine the most compelling evidence for the bull case. It’s easy to feel wise looking in the rear-view mirror. After a big correction, it’s remarkable how many investors seem to wonder, out loud, how anyone could have missed the “obvious” signs.

Reality is rarely binary to live through, though. Even in the most manic market environments, there are also always real, bullish reasons that rationally appear to support the hype. As there are today.

In the last several months, stock market outperformance has primarily come from real underlying strength. First quarter 2026 earnings were generally resilient, and in some cases, genuinely impressive. For instance, Q1 blended earnings growth for the S&P 500 was 28.4%, the strongest growth rate since post-COVID Q4 2021. Information technology earnings grew 53.4% year-over-year, with semiconductors and semiconductor equipment up 107%. Alphabet (the owner of Google) grew revenue 22% year-over-year to $109.9 billion, while Amazon grew revenue 17%. These are start-up growth rates being delivered by mega cap companies.

The potential longevity of the AI boom has also surprised some investors. Historically, many of the industries at the center of the current CapEx cycle—whether semiconductor players or advertising-based businesses like Google and Facebook—have been cyclical. Recent earnings and contract announcements are making some people question what might be possible here.

For example, Focus Wealth Management’s portfolio manager Alexander MacDonald recently joined BNN Bloomberg to discuss semiconductor company Micron’s latest quarterly results. Historically, memory has been among the most cyclical businesses in technology, with periods of strong pricing typically followed by new capacity, oversupply, and margin compression. But as Alex speaks to in the clip below, Micron’s newly announced long-term agreements add to the debate around how durable this CapEx cycle may prove to be. Click here to here watch the full interview.

In short, the bull case for the stock market right now is:

• The AI revolution is real.

• CapEx spend will go on for longer than people expect.

• The companies at the center of this boom are not start-ups but behemoths with powerful moats and free cash flow, which means they can sustain heavy spending for longer.

• Because of the example of companies like Amazon, investors today are fundamentally less concerned about near-term profitability and are willing to give more time to companies to become profitable.

• Passive investing creates a buy every dip mentality in markets that is self-reinforcing.

We see the virtues in these arguments, and we certainly acknowledge the power of AI technology. There are a number of counter arguments to the above, however. They all boil down to mathematical reality.

… Versus impossible maths

No matter how attractive a company’s future is, or how powerful its moat could become, there is always a price at which the valuation makes no sense: where the math required to produce even a modest return becomes so unlikely as to be impossible.

Consider the following. Imagine a company with a 10x price-to-sales multiple. What would it take to make a reasonable return on this investment?

In 2002, co-founder and CEO of Sun Microsystems, Scott McNealy, famously played this thought experiment out for investors, when he was asked to comment on how reasonable it was for his own company to have traded at 10x Price-to-Sales. McNealy legendarily replied:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are?

You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

In short, it takes extremely optimistic assumptions sustained for a long time to be able to generate a decent return on a stock whose initiation occurs at this kind of super high multiple.

Now, it’s worth acknowledging that, while difficult and unlikely, this is neither technically impossible, nor even unheard of. A revolutionary company with a brilliant future could do it. Amazon famously did.

The real question to ask, though, is this: how many of the companies in the S&P 500 right now are the next Amazons? How many of these companies are run by entrepreneurs as ambitious and skilled (and lucky) as Jeff Bezos? How many have the same kind of massive total addressable markets?

We ask because fully half of the S&P 500’s market cap is trading at 10x price-to-sales today (see Figure 3).

To be a passive investor in the S&P 500 Index today is to make a bet that all these companies will defy long-run historical averages and become some of the greatest stock success stories of all time. We don’t know about you, but we don’t like those odds.

A second tough mathematical reality concerns second- and third-order consequences.

Right now, many CEOs are justifying their companies’ elevated valuations by pointing to the future productivity benefits that will come from AI. They argue that AI will fuel earnings growth. Let us speak plain on what this means: it is CEO speak for laying off workers and replacing them with AI.

While many of these CEOs speak as though this would be unquestionably good for economic growth, if AI does realize its potential and displace the labour force, it will not happen in a vacuum. There may yet be a gap between when old jobs are lost and new ones are created. We ask: what happens to consumption and spending within an economy when there are many people unemployed? Can these same companies keep growing at the same rate if their own customers are unemployed?

How long can this cycle last?

A third and perhaps the most important mathematical reality relates to the durability of this CapEx cycle. For most of these valuations to make sense, investment into this industry will have to grow aggressively for many, many years. How likely is that to happen?

Answering that question in full is probably beyond the scope of this already long letter. But in our view, it depends on three things. First, whether AI applications generate enough real economic value for businesses to continue to increase spending. Second, whether the hyperscalers (i.e., Microsoft, Google, Amazon, Meta and Oracle) earn acceptable returns on the extraordinary sums they are investing today. And third, whether capital markets remain willing to finance one of the largest investment booms in modern history.

The economic value of AI to organizations is probably a question of timing. On the one hand, we see huge potential in these tools, and expect them to become deeply integrated into organizations in the years to come. On the other hand, the current costs of AI spending for organizations are nontrivial, and escalating, while the near-term payoff remains weak. According to a recent survey from PwC, 81% of C-suite leaders say their companies are at least a year away from “meaningful returns” from artificial intelligence.

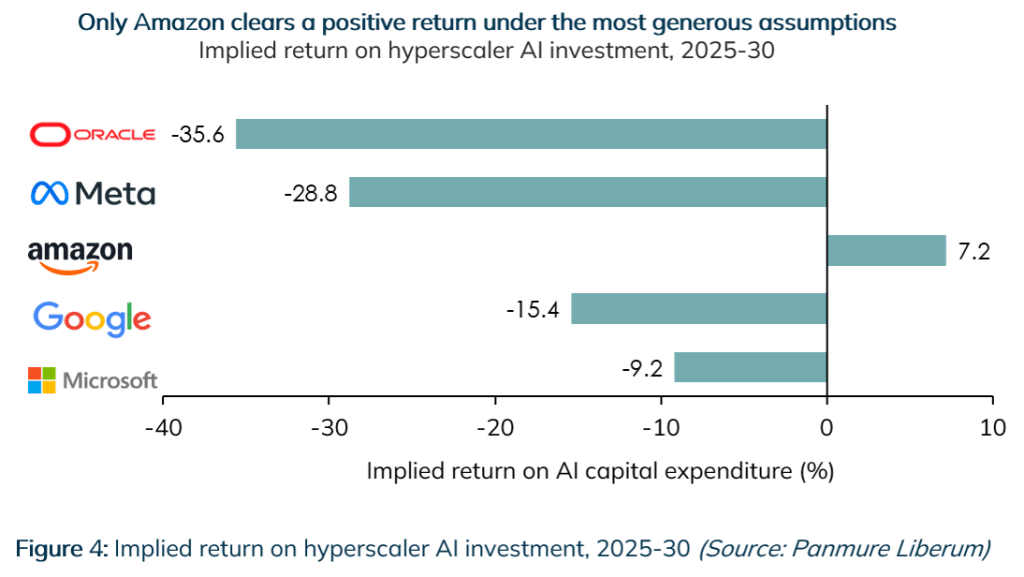

The question of hyperscaler returns is a bit clearer. None of these projects promise to generate compelling returns yet.

According to an article posted by the Financial Times in May, consensus estimates suggest the largest hyperscalers will increase capital expenditures by roughly 20% annually through 2030, an unprecedented rate of investment for companies already this large. Yet revenues are expected to grow closer to 15% annually. Even under the extremely optimistic assumption that every additional dollar of revenue carries no incremental operating cost, the implied returns on those investments are unattractive for most of the companies involved (see Figure 4).

Put another way, the amount of capital being deployed is growing faster than the amount of value expected to be created.

Then there is the question of how long these companies will maintain enough access to capital to keep investing at these rates.

U.S. businesses invested approximately $1.5 trillion in information technology equipment and software in 2025. At the peak of the technology bubble in 2000, that figure was approximately $466 billion, or roughly $830 billion in today’s dollars. In other words, the current investment boom is already dramatically larger than the Dot-Com Bubble that ultimately ended in one of the largest equity collapses in history. (Recall, the NASDAQ declined 79%).

Granted, the companies at the center of this boom are behemoths with dominant monopoly-like businesses that churn out billions in free cash flow every year. Investors have shown a remarkable appetite to fund the growth ambitions of these companies with both newly issued debt and equity. Moreover, many of them are engaging in long-term circular vendor financing agreements that effectively push out the duration of the party.

But there is always a point when the music stops.

The important takeaway here is that even minor pullbacks can have major consequences for this math. During previous technology investment slowdowns, declines of only 4% to 6% in capital spending were associated with meaningful economic weakness. Given the extent to which current U.S. growth depends on technology investment, even a relatively small pullback could have disproportionately large consequences for economic growth. And, because stocks trade off “multiples” of earnings and cash flow, the effect on stock prices could be much more dramatic.

If hyperscalers begin reducing investment plans, even modestly, the effects would ripple throughout the economy.

What risk?

In summary, by far the most important trend occurring in equity markets right now is AI. We leave calling this a bubble or not to the reader. As an investment team, however, what concerns us is not the theme so much as the psychology and behaviour around it. Not since 1999 have we seen anything like this kind of hubris or complacency.

Here are some of the traditional indicators of late-stage market exuberance:

•Historically elevated equity valuations

•Extreme stock market concentration

•Tight credit spreads

•IPO frenzies

•Circular vendor financing

•Widespread belief in growth rates far above historic norms

•Everyone believing the stock market can only go up

•Heavy allocation towards equities in households

•Financial speculation

•Belief that “this time is different”

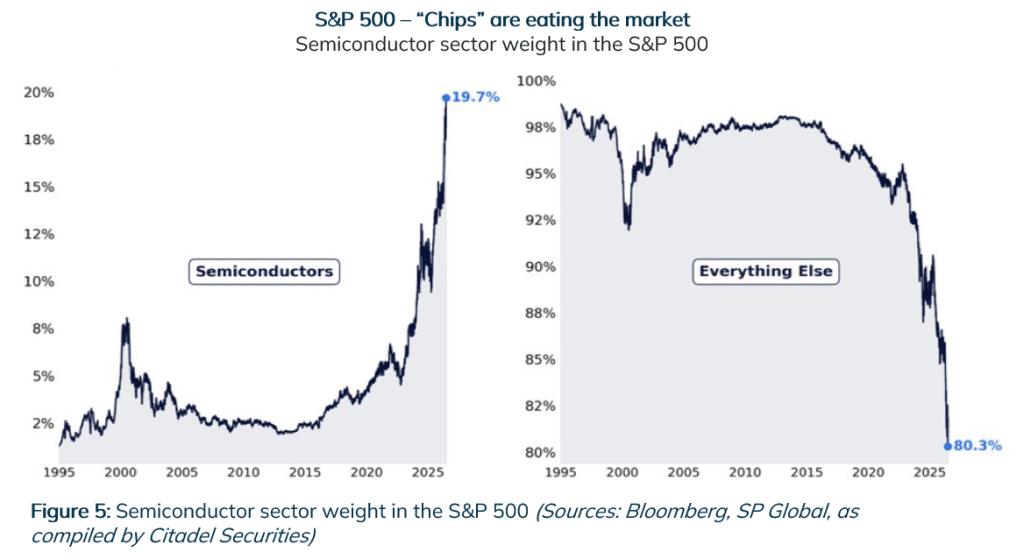

All of which are flashing red as we speak. Of particular note is concentration: AI companies now account for over 50% of the S&P 500 Index. Semiconductor companies alone now account for as much as 20%.

Figure 5 below shows just how extreme the recent surge in semiconductor stocks has been. Where semiconductor stocks used to represent roughly 2% of the S&P 500 index, today they are closer to 20%.

Portfolio positioning

What do we recommend in this environment? What we always do, with a little more caution. Investing in companies where a compelling investment case can still be made. Diversifying across many kinds of uncorrelated assets. Remaining focused on the fundamentals and remembering discipline, even as everyone else abandons theirs.

We would also note that, although it may be tempting to move to extremes at this point—either abandoning principles and joining the party, or exiting the market altogether—history has not been kind to either of these approaches. We continue to advocate for portfolios built on timeless investment principles that advance regardless of the period in the cycle.

To this point, even in this environment, there remain compelling investment opportunities.

Equities

Similar to 1999, today the oxygen is being sucked out of the rest of the market in order to fuel the AI CapEx buildout. One important lesson from the 1999/2000 period is to avoid the parabolic moves and concentrate on the high-quality businesses that had been the “source of funds” to fuel the bubble.

In Canada, we are finding a number of compelling opportunities, including many high-quality businesses that have either been left behind by the market’s enthusiasm for AI or are being overly punished by fears of it. During the quarter, we initiated a position in Montreal-based engineering and professional services firm WSP Global, whose shares have come under pressure amid concerns that AI will erode demand for engineering services. We believe those fears are overstated. While people are willing to let AI write emails for them, we don’t think we are yet at the stage where we trust AI to build bridges.

Moreover, as a firm with significant exposure to power infrastructure, data centers and other large-scale capital projects, WSP appears well positioned to benefit from many of the same trends driving AI investment, as well as renewed government commitments to infrastructure spending. We believe this combination of a high-quality business, favourable long-term tailwinds and an attractive valuation creates a compelling investment opportunity.

In the United States, we continue to see selective opportunities in health care. The sector has been under pressure and has largely sat outside the center of market enthusiasm. During the quarter, we initiated a position in Abbott Laboratories, a diversified healthcare company with leading franchises across medical devices, diagnostics and nutrition. Recent operational challenges have weighed on the share price, but we believe many of these issues are temporary rather than structural. The company has increased its dividend for more than 50 consecutive years, continues to invest heavily in innovation and, in our view, offers an attractive combination of quality, resilience and valuation.

We also added to Home Depot. While elevated mortgage rates have driven U.S. housing turnover to historically low levels, creating a cyclical headwind for renovation spending and sentiment toward the shares, we believe those pressures are unlikely to be permanent. Home Depot remains one of the highest-quality retailers in North America, with exceptional returns on invested capital, a dominant competitive position and a business model that should benefit as housing activity gradually normalizes.

We have also maintained dry powder to act on volatility. If volatility returns and high-quality businesses trade at more attractive prices, we want to be in a position to put capital to work.

Fixed income

Within government bonds and corporate credit, we remain careful. Credit spreads are tight and leave little margin for error. In this part of the portfolio, we continue to emphasize high-quality issuers and shorter-duration securities while remaining patient for more attractive opportunities should markets become more dislocated.

Alternatives

Finally, alternatives continue to play an important role in portfolio construction. We continue to favour strategies that provide differentiated sources of return and diversification from traditional public markets. While no asset class is immune to periods of volatility, thoughtfully selected alternative investments can improve portfolio resilience and broaden the opportunity set available to investors.

This kind of buffer is more important than ever.

Final thoughts

This appears to be a once-in-a-generation moment. It is different, in the ways in which technological revolutions always usher forward novel inventions and conditions. AI has all the potential to become one of the most profound technological advancements ever. But it is also the same, in that it is inciting the same primal human behaviours as always. So far, we appear to be moving through a classic tech hype cycle. All the predictable markers are present.

Whether now is remembered as the beginning of a technological renaissance, another great speculative episode, or some combination of both, remains to be seen. Our job is not to predict the exact shape of history. Our job is to tilt the odds of success in favour of our clients.

This is the moment in the cycle where so much hype and social envy is present that many of those with common sense give in and capitulate.

History rarely rewards those who abandon their principles at the moment they are tested.