IPOs and the greater sin

With new index rules and blockbuster IPOs, passive investors are about to be exposed to even more valuation risk

By Kara Lilly, CFA, and Alexander MacDonald, CFA

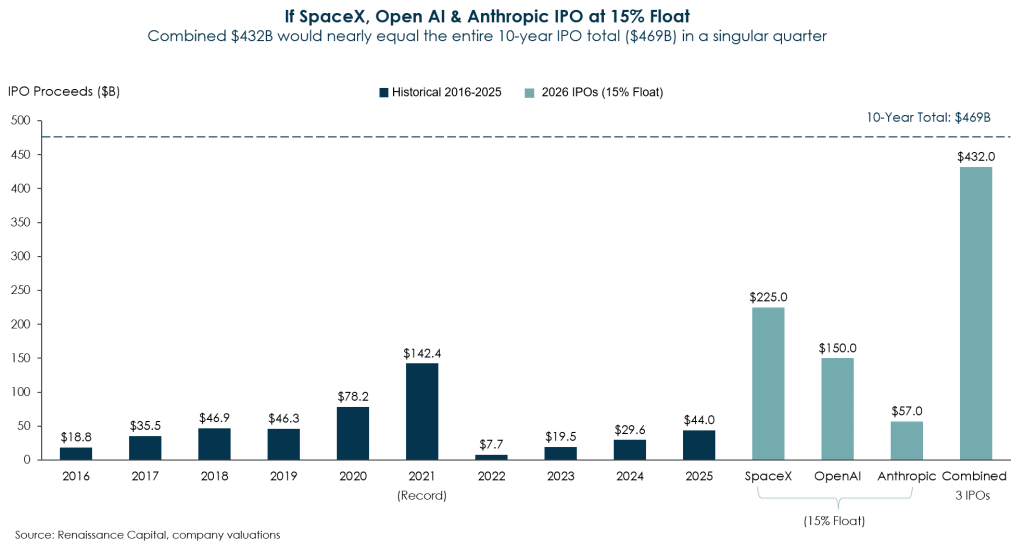

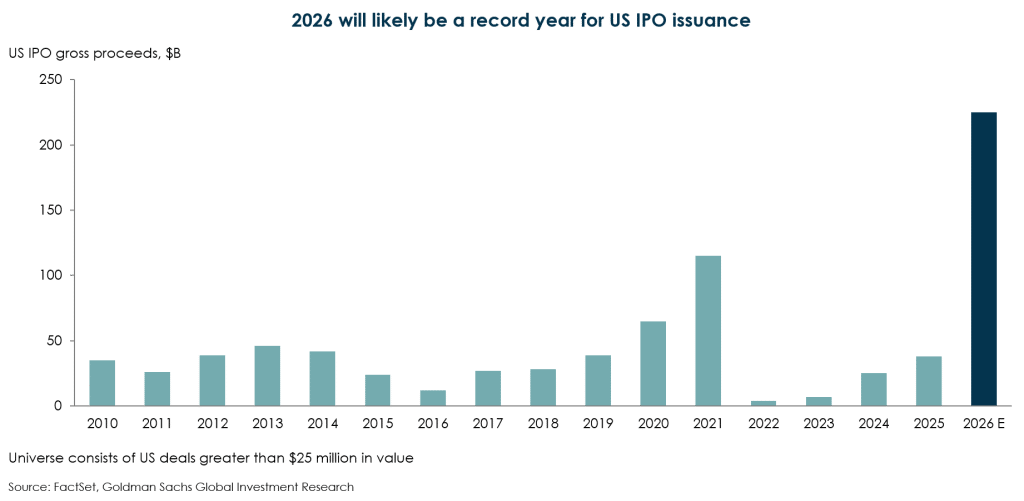

In the coming weeks and months, SpaceX, Anthropic, and OpenAI are expected to go public in a slate of unprecedented, history-making initial public offerings. Together, these companies are projected to raise between $175 billion and $245 billion and command a combined market capitalization exceeding $3 trillion. Not since the IPO frenzy at the peak of the dot-com bubble have investors seen anything quite like this.

The moment is consequential because it coincides with new index rules that would allow these mega-cap companies to be included in the NASDAQ-100 Index shortly after listing. Until recently, newly listed companies on NASDAQ generally had to complete a three-month seasoning period and meet strict liquidity thresholds before becoming eligible for inclusion in the NASDAQ-100. There was a reason for this requirement: stocks often pop, then fizzle, after their public offerings, and need time to settle. Waiting a few months before adding a new equity to an index helps ensure that prices have at least begun to stabilize before passive investors are required to hold the stock in their portfolios.

Now, however, the largest new listings can become eligible for inclusion in the NASDAQ-100 in as little as 15 trading days. There are three consequences for investors. First, as has been widely noted, passive investors in NASDAQ-tracking funds may now be forced to buy a handful of newly public stocks almost immediately after listing, potentially at extremely expensive valuations.

Second, this raises the question of errors of commission versus errors of omission in investing, and which is worse.

Third, it highlights the inherent risks of passive investing in periods of mania. Passive investing has its merits. But when the market moves to extremes — when it becomes highly concentrated, richly valued, or both — owning the index can become risky. That is especially true when one considers why many investors chose passive funds in the first place: they wanted diversification and did not want to actively follow market noise.

Far from being passive, holding an index now means making some very large bets.

What investors are being asked to buy

Before turning to the index question, it is worth asking what public investors are actually being asked to buy here. These are not normal IPOs. They are not even normal technology IPOs. Each company is already enormous, each is raising the equivalent of a small country’s GDP in capital, and each is being valued less on the current state of its business than on the belief that it may dominate a much larger market in the future.

Let’s start with SpaceX, whose S-1 filing references dinosaurs and reads like a science fiction novel in ways both good and bad. The company’s stock debuted at $135 per share on Friday in the largest IPO in history, valuing the company at roughly $1.8 trillion and making Elon Musk the world’s first trillionaire.

SpaceX is a collection of businesses. At its core is a space launch and spacecraft franchise, which generated $4.1 billion in revenue in 2025 and ran roughly breakeven in profits. Then there is the company’s Connectivity segment, which includes Starlink, a satellite broadband network, and Starshield, a government and national-security satellite business. To give credit where credit is due, SpaceX’s Connectivity business is genuinely innovative. It brings novel, differentiated products to market, is doing something no one else has shown much aptitude to do at scale, and has a dominant competitive position. Connectivity generated $11.4 billion in revenue in 2025 and, unlike much of the rest of the company, appears to be a real profit engine.

In addition to these thoroughbreds, SpaceX owns a stable of AI and social-media businesses with weaker competitive positions and more fraught investment theses. This less attractive group includes xAI, the AI company behind Grok, the chatbot; Colossus, its compute infrastructure; and X, the platform everyone still knows as Twitter.

The bull case for SpaceX stock is simple: the company has changed the economics of space, created a global communications network, and positioned itself as the central private-sector platform for an industry that could be much larger in the decades ahead.

The bear case is simpler still: the valuation is bonkers. Even if one gives Elon Musk extra credit for his ability to execute on long shots, these are mind-boggling numbers. For perspective, SpaceX generated $18.6 billion in revenue in 2025 and reported a net loss of $4.9 billion. Yet the company is trying to issue publicly traded stock at a $1.8 trillion valuation. That implies a price-to-sales multiple of roughly 96x — not price-to-earnings, because there are no earnings yet.

The other two behemoths about to IPO are Anthropic, maker of Claude, and OpenAI, maker of ChatGPT.

These two companies are frontier artificial intelligence companies. They build and operate the large models, developer tools, and enterprise products at the center of the AI investment boom. Their strengths are obvious. Anthropic has become one of the leading AI labs by positioning Claude as an enterprise-ready model family with strong demand from businesses that want AI tools for coding, writing, analysis, and workflow automation. OpenAI has the best-known consumer AI product in ChatGPT, a major developer platform, enterprise distribution, and the brand most closely associated with the generative AI revolution. In both cases, these companies are not selling a small application. They are trying to become the base layer on which other companies build.

But as exciting as these companies could be, neither has a fully solidified business model yet. Frontier model development requires staggering and recurring spending on chips, data centers, engineers, and research. Each new model cycle costs more, and the competition is relentless. Realistically, we do not know which of these companies will win yet, much less when they will be able to produce durable profits.

And now both are moving toward the public markets. Anthropic confidentially submitted a draft S-1 to the SEC on June 1, 2026, while OpenAI announced it had filed IPO paperwork on June 9. Both are expected to seek $60 billion or more.

Again, and like SpaceX, these prospective capital raises are on a scale normally associated with sovereign wealth funds, national infrastructure programs, or the largest privatizations in market history. Neither has earnings.

Presumably, when they come to market, they will also be valued aggressively on hype.

Errors of omission versus commission

This brings us to the second point: the difference between errors of commission and errors of omission, a philosophical question that is more practically relevant to the stock market than one might initially think.

In philosophy, sins of omission are failures to do what is good, right, or required (a failure “to act”). Sins of commission are, by comparison, active transgressions, involving thoughts, words, or deeds that are morally wrong. Both are often regarded as grave.

In investing, however, while an error of omission can feel like the greater sin — missing a winner may haunt you forever — it is commission that is greater. The reason is the mathematical reality of destroying capital. It is simply impossible to compound from absolute zero.

When an investor fails to act on a great buying opportunity, it can hurt, but they will survive and live to invest another day. Destroying capital, by comparison, can wipe out one’s life savings.

The investor who destroys capital exits the game.

The worst kind of investment error

This brings us to our third and final point. The upcoming IPOs are revealing in many ways, but especially in this: they highlight the worst kind of error an investor can arguably make.

An error of commission, made without knowing.

In plain English:

Making a massive bet, and not realizing you are making it.

Our team would argue that many passive investors are at risk of doing exactly this in their portfolios today. Theoretically, being a passive investor and following an index should help an investor be well diversified. Now, however, with the prices at which some stocks are trading and the way the indexes are concentrated, to invest passively is to make one big bet on AI. It is also to take on significant valuation risk.

For instance, today the top 10 holdings in the NASDAQ-100 make up 46.7% of the index. That is almost half of the index in ten stocks. Just the chip / semiconductor-equipment names listed in the top 25 — Nvidia, Micron, AMD, Broadcom, Intel, Lam Research, Applied Materials, KLA, Texas Instruments, Marvell, Sandisk, and Qualcomm — add up to roughly 32% by themselves.

The S&P 500 Index is likewise unusually concentrated. S&P’s own factsheet says that, as of May 29, 2026, the top 10 constituents were 39.3% of the index, and the largest constituent was 7.9%. Furthermore, those 10 largest names are entirely AI-oriented. This is a level of concentration not seen since the mid-1960s; right before the stock market went sideways for the better part of a decade.

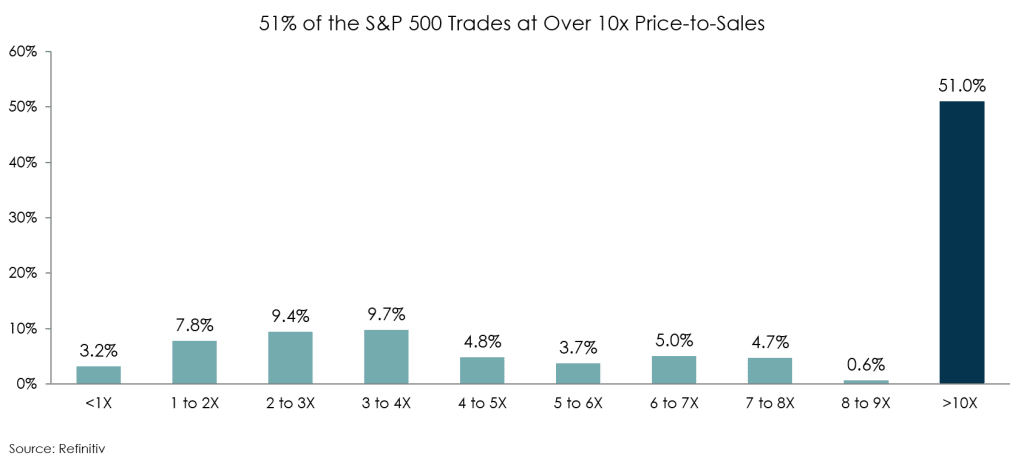

Perhaps most revealing is the fact that half of the listed companies in the S&P 500 trade at a price-to-sales multiple above 10x. Ten times sales! These are historically extreme valuations, and the assumptions required to justify them are audacious.

We are reminded of when Scott McNealy, the co-founder and former CEO of Sun Microsystems, famously criticized the 10x price-to-sales valuation of his own stock in a 2002 interview with Bloomberg:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. Zero cost of goods sold. Zero expenses. Zero R&D. Zero taxes. Zero employees. Now, having done that, would any of you like to buy my stock at $64?”

McNealy was pointing out the mathematical absurdity of investors expecting a decent return on a company trading at a 10x sales multiple. He was speaking in the cold morning after the dot-com bubble burst, as a hungover investment industry bemoaned its losses.

His words are as relevant as ever today.

Passive investing’s dirty little secret

An active manager who buys SpaceX at roughly 96x sales is making an aggressive decision. Maybe it works. Maybe it does not. But at least it is a decision. The buyer knows the thesis, accepts the valuation, and understands that they are paying far ahead for profits that may or may not arrive.

The passive investor is in a stranger position. Some might be buying the index as an active bet. But others, potentially most, may not realize they are doing anything at all. They may have bought an index fund years ago precisely to avoid stock-picking, when someone told them active investing was overpriced and dead. Now, however, they might be the unwitting owners of some of the most expensive, arguably riskiest equities in the stock market, making a bet that all the rosiest assumptions underpinning the frothiest stocks come true.

And in the case of NASDAQ-100 investors, they will become buyers of the largest and most expensive new listings almost immediately after they begin trading.

The investment industry told retail investors years ago not to overthink their hard-earned pensions, and simply to follow an index. That was a reasonable enough recommendation when mania was not so clearly brewing.

We wonder where those same voices are today. Whether they still sing the same tune. Whether they still think owning a mirror of the index is diversification.

Or whether they are actively warning passive investors about what they are sleepwalking into.