What can the US do to clean up its debt?

By Kara Lilly, CFA, and Michael Kosmalski, CFA

In 1810, at the height of France’s assault on Europe, Napoleon Bonaparte wrote in a letter to his commander-in-chief in Spain that “you must adopt as a principle that war must feed war.” The line illustrated his doctrine that military campaigns should finance themselves. But this was also a stance born of necessity. The statuesque French emperor was learning the hard way that military campaigns were expensive. France was less trusted by external creditors and had to rely on forced loans, requisitions, and plunder.

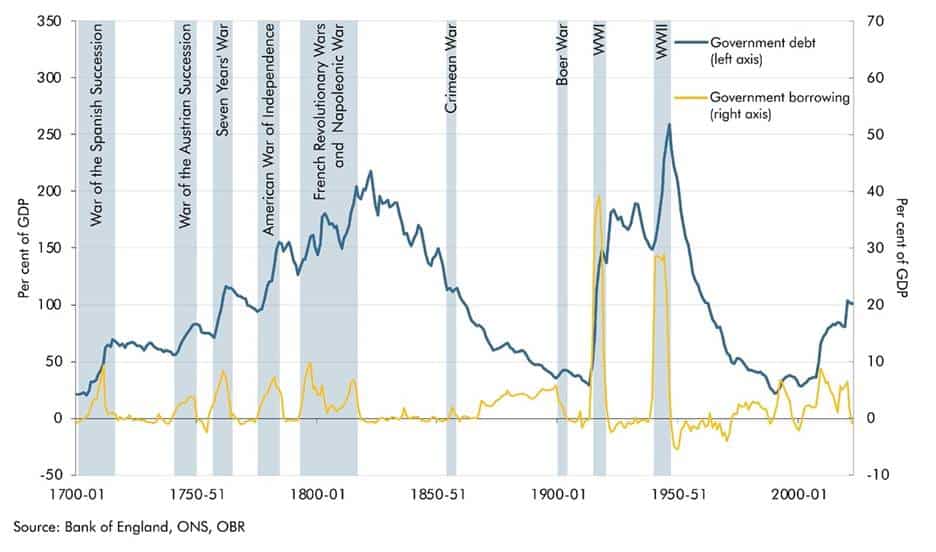

Britain, meanwhile, sworn enemy of Napoleon’s France, could issue Consols to borrow vast sums at relatively low interest rates to subsidize its army, navy, and allies. And did. According to a long-term UK public finance series called 300 Years of UK Public Finance Data, Britain took on so much debt to survive and overcome this period that, at the end of the wars with Napoleonic France in 1815, the island was left with government debt close to 180% of GDP.

However, more impressive than the load they took on was what they did next. Britain calmly and gradually paid down this debt without triggering a dramatic bond market revolt.

That the UK bond market did not flinch during this period puts it in a small and exclusive club. It also makes an interesting case study for investors. Economic systems, like physical systems, obey certain laws of physics. In the majority of cases, when a society’s rate of debt accumulation outpaces any plausible rate of repayment, the bond market loses confidence and access to credit becomes very expensive. Countries that sustain chronic deficits, say 6% or more, and pile up massive debt-to-GDP ratios, say in excess of 100%, usually face some kind of reckoning.

Three large countries in the modern era have sustained such loads without triggering a crisis and are the rare exception:

- The United Kingdom during the Napoleonic Wars and again during World War II

- Japan, almost continuously since the 1990s

- The United States, during World War II and now

Why make this observation? Two reasons.

First, America carries a heavy debt load and runs chronic fiscal deficits that would place it under immediate market pressure were it not for its reserve currency status. As of 2025, total federal debt is roughly $38 trillion, equivalent to about 122% of GDP. This is a high burden and comparable to what the country carried at the end of World War II. Meanwhile, in fiscal year 2025 the federal deficit ran at roughly 6% of GDP. More than $2 trillion was added to the debt in a single year.

Second, America’s standing in the world has shifted materially over the last year under the norm-shattering antics of President Trump. Its reserve currency status, while undoubtedly safe in the immediate future, may not be as secure over the long run. One day that status could weaken, the debt bill could actually come due, and the United States would no longer be able to punt its fiscal problems into the future. It would be forced to take some medicine.

Given everything happening in the world today, a thought experiment about these forces is reasonable for investors to make. Because whatever path they choose, America’s debt choices will impact global markets.

So, in this deep dive, we ask the following:

What could American leaders realistically do to address the debt load?

What, if any, of these actions does the Trump administration seem most inclined to pursue?

And what might this mean for investors?

UK debt loads 1800 – 2025

The levers

A little roadmap for the conversation ahead: We will begin by establishing the main ways a country can reduce its debt. Then we will introduce, and quickly dismiss, the most unpalatable and therefore least likely of these options, so we can move into a frank discussion about what Americans would hope to do versus what Donald Trump will probably try to manipulate. Ending with where we are today and how investors might prepare.

To begin, a country’s balance sheet can be distilled, if crudely, into a single ratio: debt-to-GDP. This ratio provides a quick snapshot of what a country owes and what it earns.

Sovereign Debt Load = Debt

GDP

On the top (the numerator) is the nation’s total debt. When evaluating debt-to-GDP, particular emphasis should be paid to what is owed to external creditors. Debt held domestically can, in extremis, be managed or reorganized through tools available only to sovereigns (see: Japan). Foreign creditors, on the other hand, are less accommodating and expect their principal back on time and in full.

Roughly one third of U.S. Treasury debt held by the public is owned by foreign investors, equivalent to about $9 trillion, with Japan, China, and a constellation of global financial centers among the largest holders.

On the bottom (the denominator) is Gross Domestic Product, a simplified but effective stand-in for the size and productive capacity of an economy. Imperfect as it is, GDP serves as a proxy for a country’s long-term ability to service its obligations.

Over the last decade, the United States has grown robustly for a mature economy, at roughly 4–5% nominal GDP per year, of which about 2–2.5% has been real growth, with the rest attributable to inflation.

Critically, any effective strategy for reducing a nation’s debt burden must work on one or both sides of this ratio, either by reducing the debt, increasing GDP, or some blend of the two.

Reduce / limit debt (numerator)

- Run primary surpluses (either raise taxes or cut spending)

- Default

- Restructure (functionally a default)

- Sell assets

- Yield control

- Monetization

- Financial repression

Grow GDP or inflate debt (denominator)

- Grow real GDP

- Inflate debt away

Unlikely or unpalatable

With that teed up, let’s examine a few of the “straightforward” strategies the United States could take to directly pay down its debt load, and why the Americans probably won’t pursue them.

The first and most obvious strategy would be to embrace responsible fiscal management. Imagine. Spending in line with the revenue actually generated.

Clearly, this is a sensible option. Unfortunately, sustained surpluses require either higher taxes or lower spending, both of which demand political cohesion, electoral sacrifice, and long-term discipline. This is difficult to do in peacetime and prosperity, because electorates resist austerity when the sun is shining. In downturns it is even harder, as governments are forced to spend more, not less. American political leadership currently shows next to no appetite for such adult considerations. The last U.S. president to run a sustained surplus was Clinton, nearly thirty years ago.

A second option, if one has too much debt, is to simply refuse to pay it back. To default. Or to restructure it in some way. Policies that would qualify as restructuring include extending maturities, reducing coupons, or writing down principal. One imagines that Trump, whose businesses have gone bankrupt many times across his career, would at least be curious about the possibilities here.

This option would be technically feasible for the United States to pursue but would be a total disaster if implemented. Markets almost always treat even minor restructurings as effective defaults, because creditors understand they are receiving less than promised. Countries like Argentina that default face swift and painful consequences, including exclusion from international capital markets, soaring borrowing costs, currency instability, banking stress, and often deep economic contraction.

For the United States, issuer of the world’s reserve currency, even partial default is almost inconceivable. The global financial system depends on the stability of Treasuries.

Another option might be to sell off public assets. Canada pursued privatizations in the 1990s as part of its fiscal consolidation effort, and similar measures have been used elsewhere to smooth difficult adjustments. But it is rare that a country has enough public assets to sell to meaningfully shift its long-term debt trajectory. This is especially true in the United States, a massive economy that already operates largely outside of state ownership.

Growth and Hope

Turning to the lower half of the equation, the United States could also improve its debt position by either growing or inflating its way out of the problem.

This is simply arithmetic. If the denominator grows, the debt-to-GDP ratio falls. The real economy can expand and shrink the relative size of the debt stock. Alternatively, nominal GDP can grow faster than the nominal debt stock. One can “inflate” the debt away. In that case the ratio still declines, even if real economic activity is unchanged.

Historically, both real growth and controlled inflation have played critical roles in helping countries improve their debt positions without triggering crises. After World War II, for example, the United States, the United Kingdom, and France all emerged with enormous debt burdens. But the decades that followed were characterized by powerful demographic and economic tailwinds. Reconstruction spending, industrial expansion, and the arrival of the baby boomer generation into the workforce produced rapid economic growth. Combined with moderate inflation and relatively low interest rates, these forces steadily pushed debt ratios down across the developed world.

Could the United States grow its way out of its current debt load? Under the right conditions, certainly. But several caveats should be noted.

First, it is extremely difficult to engineer economic growth beyond the economy’s natural rate. Implicit in almost every political campaign is the argument that a candidate will be good for the economy. But how often do politicians truly control growth outcomes? Macroeconomies are vast, complex, adaptive systems. They respond to technology, demographics, productivity, capital investment, and global conditions. Presidents have only so much influence over these forces.

Second, if America wants to improve its debt position this way, it is not enough to grow. The economy must grow faster than its debt.

Last year the federal deficit ran at roughly 6% of GDP. That means debt is accumulating at roughly that pace relative to the size of the economy. If inflation averages 2–3%, the United States would need to sustain real growth of roughly 3–4% or more for many years simply to stabilize, let alone reduce, its debt ratio without cutting deficits.

That is a high bar. Since World War II, the long-run average U.S. real GDP growth rate has been about 3%, and in the past two decades it has averaged closer to 2–2.3%. Sustained real growth above 4% has occurred only rarely in modern decades.

Could it happen again? Possibly. An optimist might argue that artificial intelligence and automation could unleash a new wave of productivity growth, a second Industrial Revolution of sorts. Notably, the first Industrial Revolution happened to coincide with one of the few historical episodes in which a heavily indebted state successfully managed an enormous debt burden (right after the Napoleonic wars). However, the mechanics of that growth are often misunderstood.

In the decades following the Napoleonic Wars, Britain’s economy did not suddenly surge. Estimates from economic historians suggest that real GDP per capita grew only about 0.4–0.6% per year during the early stages of industrialization, and even across the full 19th century it averaged only about 1–1.5% annual real growth.

Over this period, mechanization, steam power, railways, and the factory system steadily increased productivity and shifted labour from low-productivity agriculture into far more productive industrial sectors. But Britain also benefited from a powerful demographic tailwind. The population of England and Wales rose from roughly 8.9 million in 1801 to more than 32.5 million by 1901, tripling over the century as mortality fell with healthcare advances.

When modest productivity gains were combined with a rapidly expanding workforce, the total economy grew far more quickly than productivity alone would have done. Between the end of the Napoleonic Wars and the late 19th century, Britain’s real GDP roughly tripled to quadrupled in size, dramatically expanding the country’s tax base.

Because the government ran intermittent primary surpluses and avoided major new wars for decades, the expanding economy steadily diluted the debt burden. The debt that accumulated during the Napoleonic Wars, which had reached roughly 180% of GDP in 1815, gradually fell to around 30–40% of GDP by the early 20th century.

In other words, Britain did not solve its debt problem through a technological revolution alone. Industrialization helped, but it was only one piece of the puzzle. The country also benefited from strong population growth, fiscal discipline, the credibility of its financial institutions, yield controls (discussed below) and its position at the center of the global financial system. And they did this over decades.

In other words, if the United States hopes to follow a similar path, it will likely need to attack the problem from multiple angles rather than relying on growth alone.

Yield Curve Control and Direct Bond Market Manipulations

This brings us to yield control, monetization and financial repression—policy strategies that ultimately aim to control the yield curve and keep debt payments affordable.

Not only could these policies help the U.S. with its debt burden, we would hazard to guess that President Trump finds them, at minimum, enticing. The challenge with these policies, though, is that these “direct manipulations” can have some of the largest negative direct impacts on investors and asset markets.

What are these tools? They are efforts made by governments to control interest rates on government bonds and therefore how affordable the debt is. Although each differs slightly, they are all ultimately a direct intervention into fixed income markets, which interfere with the risk-free rate, distort market signals and shift the burden of fiscal adjustment onto savers and investors. They are also often inflationary.

Yield suppression is the deliberate effort to keep government borrowing rates below what a free bond market would otherwise demand. In the United States during World War II, for example, the Treasury and Federal Reserve agreed to cap Treasury bill yields near 0.375% and long bond yields at 2.5%, with the Fed standing ready to buy whatever quantity of government bonds was needed to enforce those levels.

Monetization occurs when the central bank buys government debt in such quantity that it effectively becomes the marginal buyer keeping the market functioning at acceptable prices. Unlike yield suppression, where private investors may still hold most of the debt, in monetization the state is increasingly financing itself with newly created central bank money.

The world became used to monetization in the global financial crisis in 2008. Japan operated a monetization policy for years through its Yield Curve Control framework, introduced in 2016, under which the Bank of Japan targeted the yield on 10-year Japanese government bonds around 0% and bought bonds when necessary to enforce that level (this was concluded in 2024).

Finally, there is financial repression. Financial repression is a broad term for policies that steer domestic savings toward government debt and keep funding costs low. This can include capital controls, interest rate caps, inflation above deposit rates, or regulations that encourage banks, insurers, and pensions to hold more government bonds than they otherwise would.

Importantly, these tools alone would be insufficient to address the U.S. debt load. They would only buy time (assuming they don’t spook foreign creditors, undoing some of their effects by weakening overall demand). They might keep the ever-burgeoning debt load serviceable.

But again, these interventions can be punitive to bond holders and distort the risk-free rate, and therefore all risk-assets including equities, along with it.

That’s important to understand because Donald Trump seems interested.

Donald Trump loves low interest rates

It is difficult to predict what, if anything, the Trump administration might ultimately do about the debt load while he is still president. He might do nothing. He might make the fiscal position worse through additional tax cuts or new wartime spending. Given the sheer velocity of policy announcements coming from this administration, and the equally impressive number of reversals that sometimes follow them, no one can say with certainty.

What we do know is this: Donald Trump loves low interest rates.

He has said so repeatedly for years. During his first presidency he openly pressured the Federal Reserve to cut rates, publicly criticized Fed Chair Jerome Powell, and argued that the United States should push borrowing costs down to match or beat other advanced economies. At various points he suggested the Fed should take rates to zero or even negative territory.

This behaviour has only intensified in his second administration. Trump has repeatedly called for lower borrowing costs and has framed the issue not only as economic stimulus but as fiscal relief. In 2025 he argued that a one-percentage-point reduction in rates could save the United States hundreds of billions of dollars annually in interest payments. He has strongly and dangerously tested the independence of the Fed.

We would also note what members of his administration are saying around borrowing costs. Treasury Secretary Scott Bessent has repeatedly emphasized the importance of the 10-year Treasury yield, the benchmark that largely determines the government’s long-term financing costs. That emphasis is notable because the Federal Reserve directly controls only short-term interest rates. Such conversation is intentional, and teases more active involvement further out the yield curve.

Bessent has also referenced a largely forgotten clause in the Federal Reserve Act stating that monetary policy should promote not only maximum employment and stable prices, but also “moderate long-term interest rates.” In practice the Fed has treated this as a byproduct of its dual mandate, but resurfacing the language is significant. It suggests an intellectual argument for policy that explicitly considers the level of long-term borrowing costs. Again, this argument opens up a wider policy tool path, and has been made deliberately.

Treasury officials have also signaled that they are reviewing the Supplementary Leverage Ratio, a post-financial-crisis banking rule that limits how much leverage large banks can take on relative to their assets. Because Treasuries count toward that balance sheet exposure, loosening the rule could make it easier for banks to hold larger quantities of government debt. Greater demand for Treasuries would tend to support prices and keep yields lower.

None of this amounts to formal yield curve control. The administration has not proposed explicit caps on Treasury yields, nor has it announced policies forcing domestic investors to hold government debt.

But taken together these signals point in a consistent direction. The administration is attentive to long-term borrowing costs, interested in policies that increase demand for Treasuries, and openly supportive of lower interest rates.

This suggests an openness to experimentation. It would not be surprising to see policymakers gradually move toward policies that indirectly suppress borrowing costs if the debt burden continues to grow.

Bondholder, beware

This brings us to investors, and what they may need to think about.

Interest payments on U.S. federal debt recently crossed the $1 trillion per year mark, making them one of the largest line items in the federal budget. Each year that deficits remain large, that burden compounds.

For now, the system continues to function. Global investors still buy Treasuries. The dollar remains the world’s reserve currency.

But those dynamics are not immutable.

As this article is being written, the United States is at war against Iran. Were everything functioning completely as normal, Treasuries and the USD should be rallying. Treasury bonds, however, have not responded as strongly as what would have been true historically.

Why is debatable. Bond holders might now be anticipating higher inflation, or increased government borrowing, and requiring (appropriately) higher compensation in yields. Alternatively, perhaps investors are reassessing Treasuries as the world’s unquestioned safe asset. Which would not be good.

For investors, there are many potential paths that could unfold ahead, and portfolios must be resilient enough to withstand more than one of them. We advocate for thoughtful diversification in many of our thought pieces, and continue to do so here.

We also need to face the reality that the investment world has changed. Not long ago, investors did not think twice about allocating heavily to long-dated U.S. Treasuries. The period between 2009 and 2021 was defined by structurally falling interest rates, subdued inflation, and massive central bank bond purchases. Treasuries sat at the unquestioned center of global portfolios.

In that world, simply owning long-duration U.S. government bonds was often sufficient to generate healthy returns for the defensive portion of a portfolio. But the environment ahead may not resemble the one we have just lived through.

If America ultimately deals with its debt burden through some combination of higher inflation, yield suppression, financial repression, a weaker currency, or persistently heavy Treasury issuance, then the assets most at risk are the ones that depend on stable purchasing power and low discount rates. In plain English: long-duration nominal claims become marginally less attractive.

Looking forward, it becomes more important to be deliberate about fixed income exposure. Duration and credit should be chosen with care, ensuring investors are being adequately compensated for the risks they assume.

Likewise, it is important to build portfolios that can protect against inflation. When governments choose the politically easy route and let inflation run a little hotter than they admit, the winners are rarely fixed coupon holders. They are often owners of scarce assets, mission-critical infrastructure, strong brands, commodity producers, and businesses that can raise prices without killing demand. Businesses and assets with pricing power.

Investors should also seriously reconsider the old assumption that bonds are always be the best ballast against equity risk. Bonds may still help during a recession or panic. But if the next decade is defined less by deflationary scares and more by fiscal dominance, supply pressure, and periodic inflation waves, then traditional 60/40 thinking may work less smoothly than it did in the last cycle. A more resilient portfolio may need several shock absorbers instead of one.

To this point, investors should think seriously about real assets beyond public markets. Infrastructure, energy assets, royalty streams, farmland, and certain forms of real estate can perform very differently from nominal bonds when inflation and fiscal stress rise. These assets either produce cash flows linked to real activity, sit on top of scarce physical resources, or benefit from replacement costs rising over time. That does not make them immune to recession or valuation mistakes, but it does make them a complimentary alternative.

In short, portfolios designed for the last disinflationary regime may need to evolve. Preserving capital may increasingly mean protecting purchasing power, not simply avoiding default.

How the cornered act

Napoleon believed war should feed war because he had little choice. Financing his empire meant extracting resources wherever he could find them.

Large debts have a similar effect on governments. As obligations grow, policy options narrow and incentives change.

Eventually, the system must begin paying for itself.

History suggests that when great powers confront large debts, the solutions they choose rarely leave creditors untouched.

Investors would be wise to remember that.