The Quarterly Focus – Q1 2026

April 2026 – Dire Strait

2026 has been defined so far by a relentless series of geopolitical events. Markets absorbed these shocks through January and February—alongside episodic Artificial Intelligence (AI) related volatility—but ultimately faltered in March amid escalating conflict in the Middle East. The war in Iran has had material and far-reaching consequences, with disruptions in global energy markets reverberating across bond yields, asset prices, and inflation expectations.

Were this any other year, the sheer number of geopolitical shifts would already have made it one for the books. In January, the United States entered Venezuela and detained its president. At the same time, tensions between the U.S. and its traditional allies intensified over America’s stated desire to annex Greenland, culminating in a moment when Prime Minister Mark Carney publicly rebuked the U.S., describing a “rupture, not a transition” in the global order. In February, the U.S. Supreme Court ruled that tariff authority rests with Congress rather than the executive branch, only for the administration to introduce sweeping new tariffs the same day.

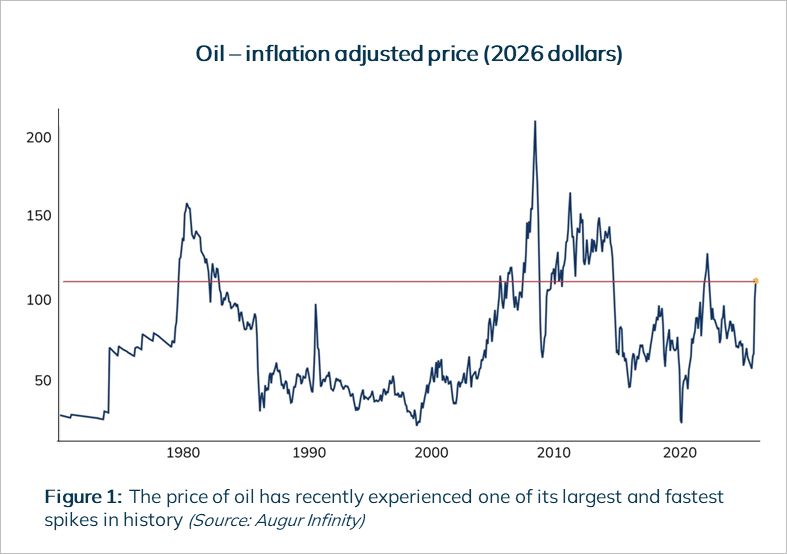

Then, in March, the United States initiated its most significant military campaign in the Middle East in decades. As Figure 1 illustrates, crude oil spiked more than 50% as global shipping all but shut down through the Strait of Hormuz. Previous expectations for Federal Reserve rate cuts dissipated, inflation expectations repriced higher, and concerns about the broader impact of the energy shock intensified. All this, and we are only in April.

Global equity markets have been, needless to say, challenged by this environment. Although the S&P 500 Index has declined nearly 4% to date, it took a last-minute tweet from the White House (announcing a possible halt to the war) to mitigate much larger losses. European equities have also generally moved lower, with broad indices down mid-single digits. Canada’s S&P/TSX Composite Index has fared better, with a roughly flat return, largely due to its outsized exposure to energy, one of the only sectors to post strong gains this quarter. Outside of the energy sector, the average Canadian stock was also off high single digits. Meanwhile, South Korea’s KOSPI Index, which had been one of the best-performing markets globally through February, fell sharply in March (-20% at its worst), highlighting the vulnerability of energy-importing, semiconductor-heavy markets to the shock.

Much is changing day to day. Trillions of dollars of capital are moving on 150-character tweets emanating from the White House.

Three observations are worth making here. The first is that a truly diversified portfolio can protect capital during volatile periods. The Focus Fund, for example, a mix of equities, bonds, and alternatives, managed to deliver a slightly positive return in a period where broader equity and fixed income markets declined. We continue to find strength and believe in the companies in which we are invested.

The second observation is to remember when geopolitics matter to investors, and when these events are just noise. As we wrote about in our most recent Quiet Investing deep dive, geopolitics matter when the rules of the game (the structure of the board) fundamentally change. However, this rarely happens. Geopolitics on its own is rarely the make-or-break factor for successful investing.

With Iran, the dust still needs to settle for anyone to understand how much has changed long-term. The immediate ripple with which we now contend is higher inflation, though how severe this becomes will depend on a number of factors.

Third, the last quarter demonstrates why diversification and thinking beyond one’s base case matters. Last year seemingly no one cared about diversification, so concentrated and convinced by the dominant AI narrative had public equity markets become. This year reminds us that the world is still governed by physical constraints as much as digital ones. Energy, supply chains, natural resources and geography all still matter. Even a desktop with the world’s most powerful AI hosted on it will need to be plugged into some source of electricity.

Moreover, in markets, there is always danger when one becomes too entranced by a singular story. The future is rarely so accommodating.

Outlook

Our portfolios haven proven resilient to the turbulence of recent times. We believe they remain well positioned to weather future chaos, while our team is ready to capitalize on opportunities created by it.

Looking forward, the odds have clearly shifted.

Last year, we spoke at length about the steep valuations in technology equities, but also more broadly across many higher-quality large cap names. Valuations had gotten ahead of themselves, and expectations left little room for error. What we are seeing now is the beginning of that excess being worked off, not through a collapse in fundamentals, but through a combination of volatility and time.

In recent months, volatility has brought some valuations back into a more reasonable range. In other cases, companies have grown into their valuations, much like a child eventually growing into clothes that once were too large. While it has occurred amid objectively harsh geopolitical developments, this is, in some respects, a healthier dynamic. It creates a broader set of investable opportunities, rather than forcing capital into an increasingly narrow group of names.

In our equity portfolios, with our stable of cash-generating, fundamentally strong businesses, we remain well positioned for the road ahead. Equally importantly, we are finding opportunities to deploy capital and make improvements around the margins. For instance, recent volatility has opened the door to reconsider high-quality large cap U.S. businesses that had previously become prohibitively expensive.

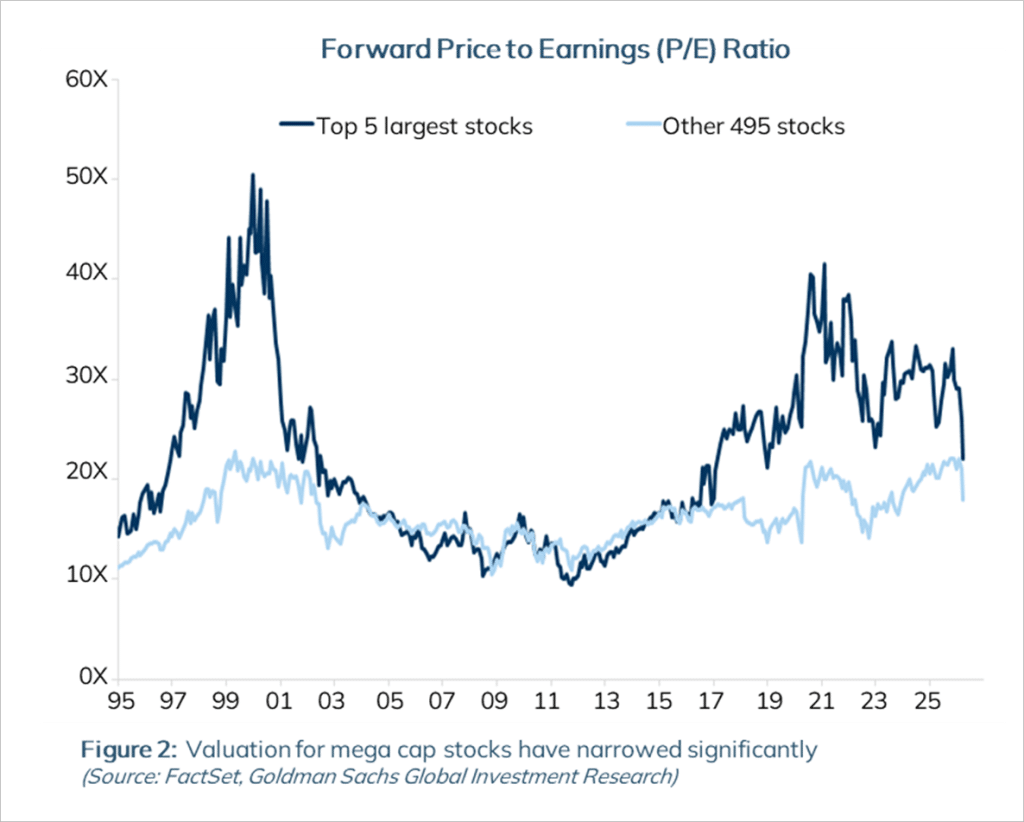

For example, Microsoft’s recent 35% decline from its previous highs has given us an opportunity to become shareholders in the company once again. Figure 2 illustrates this dynamic well. Within the S&P500, the valuation premium of the top 5 largest stocks by market capitalization has recently narrowed significantly.

Likewise, we used the selloff in February to add to high quality names that were caught up in fears over the impact of AI on software companies. This included businesses like RELX, which owns large databases of legal, scientific, and insurance information that professionals rely on every day to do their jobs; London Stock Exchange Group, which not only operates exchanges but also sells critical financial data and analytics to investors; Experian, which provides credit data and scoring used by lenders globally; SAP, whose software runs the core systems of large enterprises like accounting, inventory, and supply chains; and Euronext, which operates stock exchanges across Europe.

In each of these cases, these are businesses with proprietary data and highly recurring cash flows, where AI is likely to enhance their value rather than pose a threat.

The monetary backdrop has also shifted meaningfully. Last year saw a number of central banks around the world reduce interest rates, including the Federal Reserve, the Bank of Canada, the Bank of England and the European Central Bank. This year, the inflationary impulse from the energy shock has complicated that path. Expectations for rate cuts have been pushed out, and in some cases reversed, as markets reassess the persistence of inflation.

Clearly, the conflict in Iran is inflationary. 20% of global oil and a huge share of LNG and NGL exports (ethane, propane and butane) pass through this region, as well as critical inputs such as ammonia, urea, sulfur, and phosphates, which underpin both global food production and a wide range of industrial processes. These higher energy and material costs will feed directly into inflation, raising costs in transportation, manufacturing, food production, semiconductors and broader supply chains.

Exactly how much inflation we get will depend on the severity of the damage in the region, as well as interaction with other forces, most notably AI. Advances in automation continue to reshape labour markets, increasing efficiency and reducing the need for incremental hiring in certain sectors, which creates the potential for excess capacity and less wage-driven inflation over time. That said, AI impacts on labour markets are nascent and unlikely to counteract the near-term inflationary force from Iranian energy and supply disruptions. On balance, we expect inflation to move higher from here.

Bond markets are already beginning to reflect this tension. Yields are caught in a tug of war between rising inflation expectations and the growing risk that this same energy shock slows economic activity, potentially pushing economies toward recession. This creates a difficult backdrop for policymakers. Tightening too aggressively risks exacerbating a downturn, while easing too early risks entrenching inflation (like in the 70s). Central banks have a tough decision to make and any policy error at this stage could prove to be damaging.

Given this backdrop, we are approaching fixed income with caution. Credit spreads remain relatively tight and do not, in our view, adequately compensate for the many of the macroeconomic risks. As a result, we have been very cautious adding incremental credit risk and have positioned our fixed income holdings defensively.

Finally, the case continues to be made for investing in well-selected alternative assets. In an environment where publicly traded equities and bonds might become challenged by macroeconomic conditions, and potentially even some stagflation (an environment characterized by tepid growth and higher levels of inflation), alternatives provide an additional layer of diversification. Real assets, in particular, stand to benefit from inflationary pressures, while other strategies, such as absolute returns strategies, can take advantage of public-market dislocations created by volatility.

To date, alternatives have done their job in client portfolios, and we continue to view a role for them.

Final thoughts

George Orwell once wrote that “to see what is in front of one’s nose needs a constant struggle.” He was writing about how difficult it can be for people to confront reality as it is; how they will ignore what is plainly in front of them when it conflicts with what they would prefer to believe, choosing instead to collapse the facts into simpler narratives. Confronting reality, in his view, required active, conscious effort.

In markets, the reality investors struggle with most is uncertainty. It is human nature to prefer certainty over the discomfort that comes with ambiguity. Our instincts push us toward singular narratives, rather than the more difficult task of weighing multiple plausible paths at once, even when we know the former approach to be intellectually dishonest. This tendency has played out repeatedly across history, and it likely will continue. We saw it clearly last year.

Today, unfortunately, uncertainty feels higher. We do not know how the war in Iran will unfold, or what the lasting consequences will be. We do not yet know how the AI arms race will develop, who the ultimate winners will be, how industry will be eventually disrupted or how society will digest it all. What we do know is that both forces are large, consequential, and still evolving. This has left many investors on edge.

But this is the point that is often missed: investors do not need to know exactly how these forces will resolve to be successful. In our experience, it is entirely possible to build portfolios that can both protect and grow capital across a wide range of outcomes. This is, and remains, our mission.

Last year, many investors effectively abandoned intellectual honesty out of the magnetism of the latest technology hype cycle. Diversification was dismissed in favour of increasingly concentrated exposures, often tied to a single dominant narrative. In some cases, this was done knowingly. In others, it was a byproduct of passive structures that naturally reinforce what has already worked, but which can ultimately expose portfolios to more brazen risk taking than is potentially appropriate. We struggled with what we were seeing then, and said so.

If anything, the events of this quarter have served as a reminder that markets are complex, adaptive, and ever changing, and that the future rarely conforms to a single, clean story.

Far from being a concession, diversification honours the way the world actually works.