The Quarterly Focus – Q4 2025

When the Sirens Sing

2025 ended on themes that defined much of the year. Stock indices were up globally, led by a handful of large-cap technology and AI-related companies in the U.S., and banks and gold-related businesses in Canada. Valuations in both equities and fixed income remained historically elevated, with public equity indices such as the S&P 500 trading at roughly 22x forward earnings and corporate credit spreads compressed near historical lows. Only four times in the last 100 years have stock markets been so expensive. Furthermore, the current level of stock market concentration is among the highest in decades.

Yet nothing broke. Markets and the financial systems beneath them continued to function despite outlier conditions and occasional alarm bells. Against this strong market backdrop, our diversified portfolios delivered a return at the high end of their long-term targeted ranges, but admittedly, larger gains were had elsewhere by those holding riskier, equity-oriented portfolios.

With a new year now upon us, it is worth stepping back from the noise. Market conditions today are not “normal”; or rather, they are normal insofar as markets periodically succumb to pervasive moods of hype. There is froth and excess in the stock market, especially around companies related to AI. Unfortunately, rather than encouraging temperance, periods like this have a way of feeding on themselves. The longer this goes on, and the more that brazen, speculative bets pay off in the short run, the more pressure investors will feel to abandon discipline and chase whatever has been working. History suggests that these phases last longer than those with sense would care for. They do not end gently.

As ever, our objective at Focus is to protect and build client wealth over many economic cycles. Our approach centers on the disciplined execution of timeless investment principles: owning real businesses with high-quality cash flows, identifying underappreciated bottom-up opportunities, and constructing multi-asset portfolios that provide genuine diversification. We follow this approach because it makes sense to, and history consistently shows it to be the most reliable way to build wealth over time. There are times, however, when this approach seems out of step.

Heading into 2026, the team remains confident in the businesses and investments we own, and selective in the opportunities we pursue. This is the point in the cycle when those who fare best are the ones who anticipate temptation and prepare for it in advance.

A generational moment

In Homer’s Odyssey, the hero Odysseus is warned of the Sirens—creatures whose song is so beautiful and persuasive that sailors, drawn toward it, steer their ships onto the rocks and are destroyed. Odysseus wants to hear the song without succumbing to it, so he does something unusual: he orders his crew to bind him tightly to the ship’s mast and to stop their own ears with wax. As the Sirens sing, Odysseus strains against the ropes, desperate to follow the sound, but the mast holds. The ship passes safely through. He resists temptation by anticipating and planning for it.

Recently, it has occurred to us that while we, and many of our clients, still vividly remember what it was like to live through the late 1990s tech bubble, many investors today do not. It is now over twenty-five years since society faced a profound technological shift (the Internet then, AI now). 25 years since valuations and market dynamics exhibited such characteristics. In short, an entire generation has come and gone within the investment industry. So, while some of us remember the 90s and its aftermath, many other investors will not know or will have forgotten what it feels to be part of a hype cycle. Much muscle memory has been lost.

A reading of history would suggest very muted equity returns from here. Unfortunately, the average investor has his or her foot squarely on the accelerator. They are unfamiliar with siren songs.

But there are other ways to win in markets than blindly following the crowd.

MARKET SPOTLIGHT: stocks valuations have changed, presenting risks and opportunities

Key takeaways:

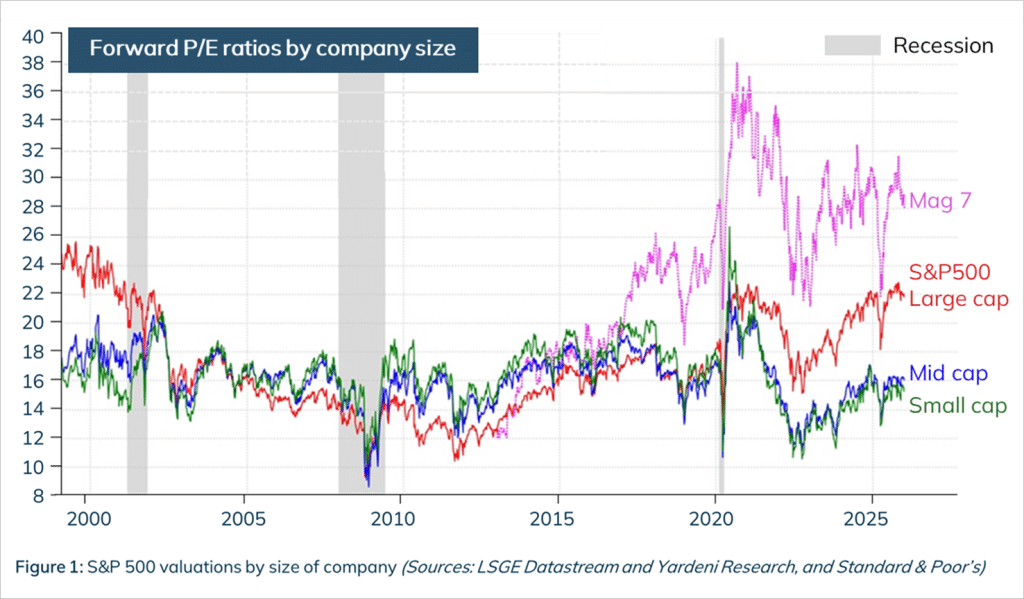

- Figure 1 shows Price/Earnings (PE) valuation multiples over 25 years for small, mid and large cap stocks, as well as the Magnificent 7 group.

- Stocks have had a good run over the last 10 years and valuations aren’t what they were 10 years ago.

- Valuation expansion is a feature of bull markets: investors get lulled into complacency – simply “paying more” in later stages.

- Right on cue, over the last 10 years the PE multiple of the S&P500 expanded by 30%, while collectively, Mag 7 valuations increased by 70%. Yet valuations for small and mid-sized companies have actually contracted by 10%.

- The last time we observed a similar level of valuation “dispersion” in the market was 1999/2000.

- Read to the end of the article to see how that turned out.

Equities Outlook

As mentioned, this year’s rally was led by a handful of large-cap technology and AI companies in the United States, alongside gold and bank stocks in Canada. Perhaps less appreciated was the strength in global stock markets, which in most cases outperformed the US. Focus’ International Equities Fund was up over 29% during the year. Our three equity strategies all delivered returns above long-term targets, however our cautious posture resulted in us “leaving the party early” while the rest of the market seems to be “partying like it’s 1999”.

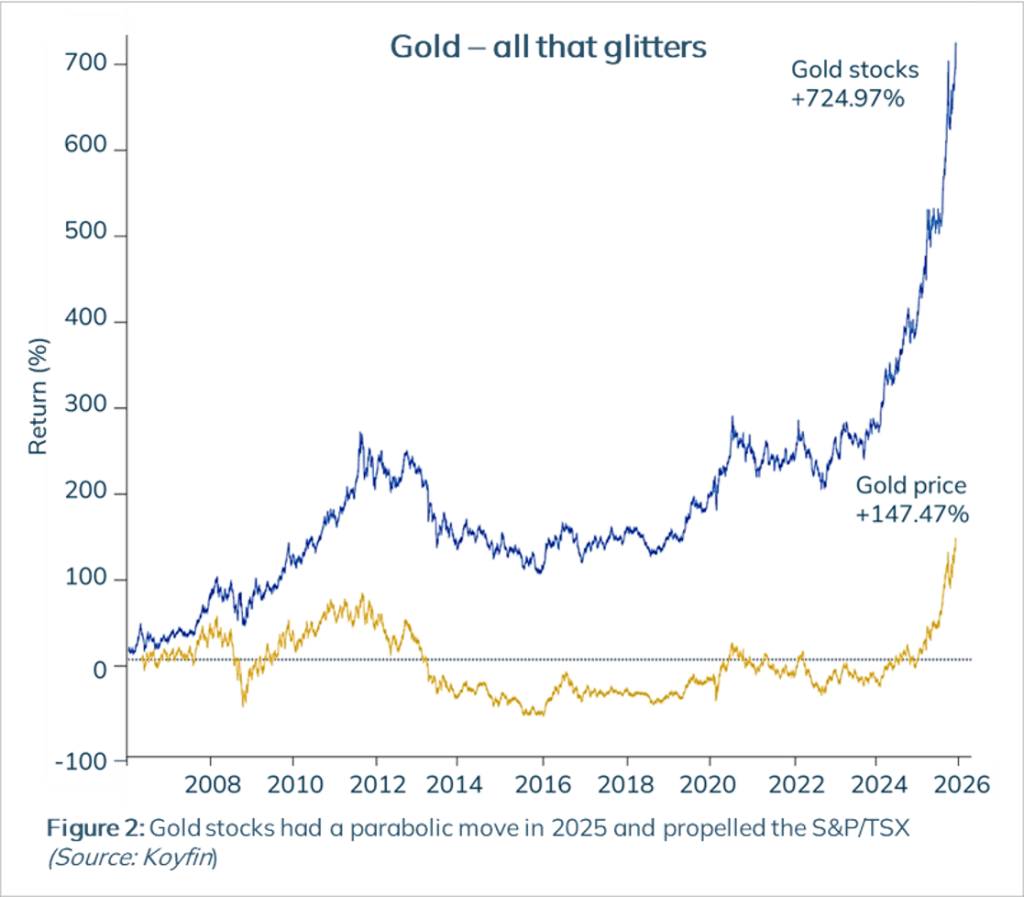

In Canada, another once in a generation moment occurred, this time with gold-related equities. After doing very little for more than a decade, gold became one of the defining “risk-off” expressions of the year, rising by over 60% from mid-$2,000s per ounce to well above $4,000 at the peak. This move was not driven by jewelry demand or any sudden industrial use, but by waning confidence in the U.S. dollar. As President Trump implemented policies that altered the geopolitical and trade landscape, the U.S. dollar weakened against a basket of major currencies, central banks diversified reserves away from U.S. financial assets and gold benefited accordingly.

Gold mining companies delivered outsized equity returns as a result. Canada’s S&P/TSX Composite Index—which, by end of 2025, had roughly a 13% weighting to gold and precious metals, by far the highest of any major equity index globally—rose approximately 29%. For context, materials represent only about 1.8–2.1% of the S&P 500. This concentration feels normal to Canadian investors who are accustomed to it but would be highly unusual in most other major equity markets.

Closing the year, the Focus Core Equity fund held approximately 4.5% in gold stocks. While our team has been constructive on gold overall, our exposure to gold mining companies via direct equity investments has been tempered by the low-return nature of these business models, as well as our belief that businesses with stronger innate compounding characteristics exist elsewhere. Gold miners can be difficult, capital-intensive businesses, and rarely generate returns on capital that exceed their cost of capital across full cycles, but clearly that was not the case in 2025 (see Figure 2).

The strong performance of the TSX was also supported by capital flows back toward Canada and away from U.S. markets, particularly into Canadian banks—often the first port of call for money flowing into Canada. Canadian bank stocks delivered strong results in 2025, and our bank holdings RBC and Scotiabank performed well. It is important to caution however, the big 5 Canadian banks are approaching the high end of their historic valuation range and as a general rule, Canadian investors are over indexed to this group which makes up over 30% of the Canadian market.

Looking ahead, we look for companies where a reasonable investment case can still be made, without holding one’s nose or resorting to the rosiest growth expectations. As we have noted in past letters, many of the companies that have recently performed well are now trading at valuations that require essentially everything to go right and nothing to go wrong to register even a modest return. One JPMorgan study shows that stocks trading at these multiples typically result in 5–10-year annual returns in the low single digits.

So where are we finding opportunity? In unexpected places, with unsexy or unfamiliar names; in businesses that sell everyday necessities, generate steady cash flow, and are largely ignored during periods of market excitement. One such example is Jamieson Wellness.

Jamieson Wellness is one of Canada’s leading producers of vitamins, minerals, and nutritional supplements. If you have ever walked down the supplement aisle of a pharmacy, grocery store, or big-box retailer, you have likely seen Jamieson products. The company sells branded vitamins such as vitamin D, multivitamins, probiotics, and immune-support products that consumers buy repeatedly as part of daily health routines. Jamieson’s business is simple and durable. It formulates and manufactures supplements, distributes them through major retailers, and benefits from strong brand recognition built over more than a century. This is not a fad-driven business. Demand is driven by aging populations, rising health awareness, and routine replenishment. People do not “upgrade” vitamins every year, but they do keep buying them.

Importantly, Jamieson is not just a Canadian story: they are a growth company, with metrics rivaling any Mag 7 tech company. Over the last five years, the company has expanded internationally, doubling both revenue and EBITDA. The U.S. and China now account for nearly half of Jamieson business. While Jamieson does not attract attention during speculative market phases, it generates consistent cash flow and compounds value steadily over time: exactly the type of business that tends to be overlooked when markets are focused on excitement rather than fundamentals.

Another example is Drax Group.

Drax Group plc is a UK-based power generation company that plays an important but often overlooked role in Britain’s energy system. To understand Drax, it helps to think about how electricity grids actually work. While wind and solar power increasingly feed the grid, their contributions are intermittent; you cannot count on them to produce electricity exactly when demand is highest. Drax helps solve this problem by providing dispatchable power, meaning it can generate electricity on demand when the grid needs it.

Drax operates one of the UK’s largest power stations and currently supplies roughly 6–7% of the country’s electricity, making it strategically important to energy security. The company generates power primarily using sustainable biomass and controls much of its fuel supply itself, which supports stable operations and cash flow.

Despite this, Drax trades at a low valuation—about 6.5x earnings—and offers a dividend yield of approximately 3.4%. The business generates significant free cash flow and is expected to produce roughly £3 billion by 2031, compared to a current market value of about £2.7 billion. While government support for the power station is scheduled to end in 2031, the market appears to assign little value beyond that date. We believe this overlooks the long-term value of Drax’s assets, including its scarce grid-connected site and the potential to extend its life through long-term power contracts, such as supplying electricity directly to data centres. There will be no AI without companies like Drax.

“ When markets reward concentration, speculation, and hype, it becomes increasingly uncomfortable to remain patient and selective.

In both Jamieson and Drax, we see businesses that are essential to everyday life, and priced as though their futures are far less durable than we believe them to be. These are not the kinds of companies that dominate headlines. But historically, they are often the ones that quietly deliver strong long-term results.

Fixed Income Outlook

If equity markets in 2025 were defined by concentration and enthusiasm, fixed income markets were defined by tension. Throughout the year, central banks walked a narrow path between tepid growth and persistent inflation pressures. As the Bank for International Settlements has noted, global monetary policy now operates in an environment shaped by high public debt, geopolitical fragmentation, and structural inflation risks that did not exist in prior cycles.

Interest rates declined modestly over the year, but the path forward remains uncertain. A case can be made for weaker growth and lower rates, particularly if economic growth rates remain tepid. At the same time, inflation risks are real. This is especially relevant in the United States, where President Trump has openly floated the idea of yield control measures, which, if implemented, could distort bond markets and encourage both a weaker dollar and inflation.

In this environment, we are prudent around duration risk and highly selective in the credit we own. That said, opportunity still exists. One such example is Spectrum Brands.

Spectrum Brands is a global consumer products company whose brands are found in millions of households. Its portfolio includes everyday essentials across pet care, home and garden, personal care, and household products. Examples include pet nutrition and supplies, lawn and garden products, grooming tools, and small household appliances: items people continue to buy regardless of economic cycles.

In recent years, Spectrum’s results have been weighed down by a series of external headwinds: the post-COVID normalization of demand, aggressive inventory reductions by large retailers, pressure on consumer spending, input cost inflation, and most recently tariffs on Chinese imports. Together, these forces compressed margins and hurt reported earnings, causing the company’s bonds to sell off materially.

We view these challenges as largely cyclical and temporary rather than structural. Importantly, the company has responded by strengthening its balance sheet and prioritizing liquidity. Adjusted leverage is down significantly from prior years, and the company is expected to generate roughly $150 million of free cash flow, compared to an equity market capitalization of about $1.4 billion. This improved financial footing leaves Spectrum far better positioned to navigate normal economic volatility.

We purchased Spectrum Brands’ bonds in June at a price of 80.25, equating to a yield to maturity of approximately 8.25% through 2031. In our view, this yield more than compensates us for the risks involved, particularly given the company’s essential product mix, improved balance sheet, and ability to generate cash through the cycle.

Alternatives Outlook

In an environment like this, where equity markets and other risk assets have already run at full speed, it can be tempting to question the need for alternative investments. When the stock market is ripping, diversification can feel unnecessary. In reality, this is precisely the point in the cycle when having these assets in place matters most.

Alternative assets are designed for periods marked by elevated valuations, concentrated market leadership, and greater uncertainty around future returns. Real estate and infrastructure, for example, can be particularly valuable in environments where growth is uneven, inflation remains a consideration, and traditional assets are more sensitive to shifts in interest rates or investor sentiment (like, for example, the peak of a hype cycle). Their returns tend to be supported by contractual income, long-term demand, and tangible underlying assets rather than broad market momentum.

Broadly, alternatives provide exposure to different drivers of return—such as income, asset-level cash flows, or specific opportunities—rather than the direction of public markets alone. Clearly, some of this is what we want right now.

Our team remains confident in our alternative investments, and they continue to do their job in client portfolios.

Final thoughts

Periods like the one we are living through test investor discipline. When markets reward concentration, speculation, and hype, it becomes increasingly uncomfortable to remain patient and selective. The siren songs grow louder, and the pressure to abandon process intensifies. But it is exactly when everyone else abandons their principles that holding true to ones’ own matters most.

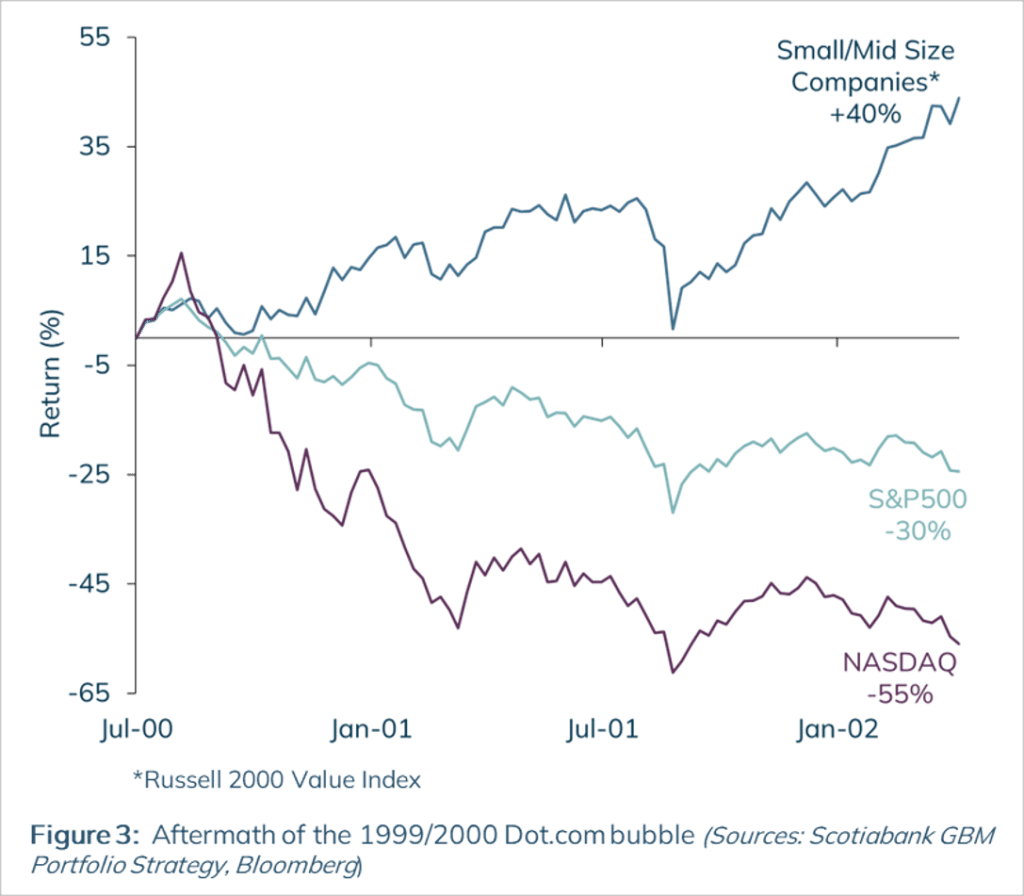

As we enter 2026, we do not know when today’s excesses will unwind, or what form that adjustment will take. We would note that every major technology hype cycle in modern market history has been followed by a material market correction; that there are critical parallels in this moment to the Dot Com bubble, and technology hype cycles before this; that equity valuations at some of these extremes would imply low single digit returns, or worse; and, that we are seeing more and more signs of the FOMO (Fear Of Missing Out) one would expect later in the cycle.

Figure 3 illustrates what the aftermath of the Dot Com era of 1999/2000 looked like. In short, the hype cycle went into reverse, while thoughtful, fundamental investing reasserted itself.

We remain confident in the businesses and securities we own, cautious where risks are poorly compensated, and ready to act where opportunity presents itself. This is not the moment to chase the crowd. It is the moment to win elsewhere and ensure the ropes are secure.