The Quarterly Focus – Q1 2025

The following is an excerpt from the quarterly newsletter distributed to clients.

The Great American Reckoning

Markets entered 2025 on familiar footing—buoyed by excitement over artificial intelligence and an entrenched faith in American exceptionalism. By February, however, that fever pitch had broken. U.S. stocks fell sharply as investors weighed inflation concerns, pending tariffs, and a slowing economy. Technology and large-cap U.S. stocks—market darlings only months ago—tumbled from historically lofty valuations. Meanwhile, stock markets in Europe and China, long dismissed as stagnant, experienced strong relative performance: MSCI Europe and MSCI China were up 10.6% and 15.1 respectively, while the S&P 500 fell 4.3%. Canada’s S&P/TSX Composite was up a modest 1.5% against this backdrop.

In short, this quarter was a remarkable change in pace and tone from the hubris that had defined the end of 2024. Major geopolitical tectonic plates now shift beneath global markets. The catalyst? In a word, or—a name: Trump.

Since taking office in January, President Trump has unleashed a bewildering series of policies that have thrown global markets into disarray. He kicked things off with a trade war targeting Canada, Mexico, and China. Not long after, he endorsed a potential U.S. debt restructuring under the so-called “Mar-a-Lago Accord”—a prospect the bond market, unsurprisingly, greeted with hostility. He also threatened to annex Greenland and, publicly sided with Russia in the war in Ukraine, so alarming Europeans that even Germany, long committed to fiscal restraint, responded by amending its constitution to allow a major ramp-up in military spending.

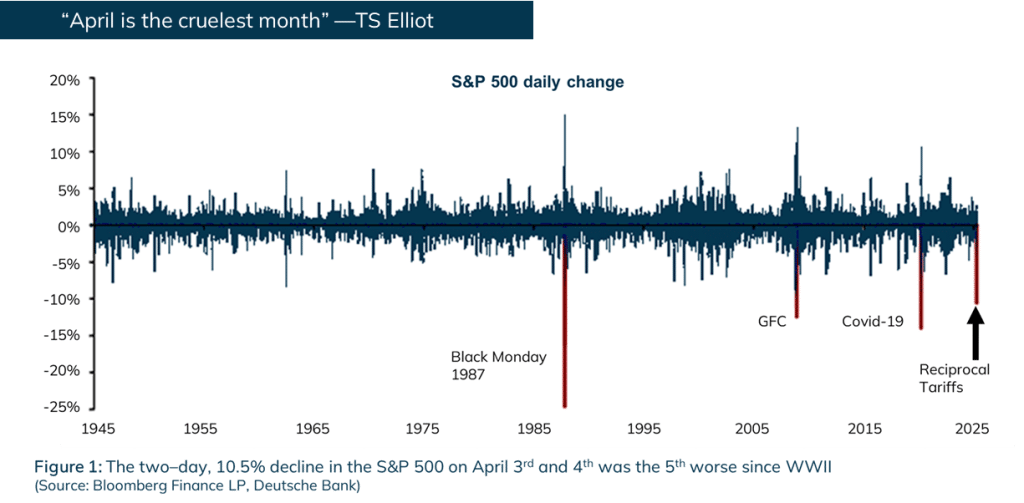

Then came the April 2nd announcement—dubbed “Liberation Day”—of a 10% baseline tariff on all imports, alongside sweeping reciprocal tariffs on dozens of trade partners. The move marked the most aggressive protectionist shift since the Smoot-Hawley Tariff Act of the Great Depression.

In just two days, the S&P 500 shed more than $6.5 trillion in value—its fifth-worst two-day drop since World War II. The dollar weakened, Treasury yields surged, and for the first time in decades, markets began to question the U.S. dollar’s safe haven status.

(As this letter goes to print, Trump has announced partial tariff relief, and some of the market losses have been clawed back.)

Taken together, these actions are set to challenge global growth, fuel inflation in the U.S., and shake the foundations of the existing world order. The resulting uncertainty is so profound that many businesses have simply hit pause, waiting for policy direction. Sovereign nations worldwide, including Canada, are waking up to the reality that the U.S. is no longer a reliable trade or security partner. As Canadian Prime Minister Mark Carney put it, the old ways are “over.”

Moments like this require investors to take a real step back— to take in the full picture, and to ground themselves. Uncertainty is obviously high right now. A rather large rock has been thrown into the global economic pond, which is already causing real, and painful, economic ripples. But it’s also worth noting that the world is in flux, not ending, and as challenging as the next few months may be, the strongest businesses and most capable leaders will adapt and survive. Moreover, as ever, market chaos should present compelling medium and long-term opportunities for discerning investors. This happens to be the business we are in at Focus. Being discerning, being ready. For moments, like now, when it counts.

On this note, our investment team believes in the businesses and managers in which we are invested— our portfolios are built off the backs of high-quality, well-run companies— and the resilience created from our multi-asset portfolios. Although this environment and its uncertainty naturally make us cautious, this is also why we build portfolios the way we do. It is worth noting, for example, that our alternative investments are doing exactly what they should be doing in this environment: being ballasts to client portfolios. Our multi-asset portfolio, the Focus Fund, was up 3.3%, on the quarter.

We stand ready to deploy capital into compelling opportunities, and also, tread carefully.

Equities

As alluded in Figure 1, equity markets in Q1 reflected a tale of two markets. What began as a continuation of American enthusiasm and AI hype quickly morphed into concerns around U.S. growth, inflation and President Trump’s tariff plans. By late January, markets were being whipsawed by President Trump’s will-he, won’t-he decision making towards Canadian, Mexican and Chinese tariffs. The mood also began to sour on January 27, when the sudden and dramatic demonstration of DeepSeek R1, a Chinese-developed AI model, stunned global markets and suggested a serious narrowing of the AI capability gap between the U.S. and China.

In short, after a major run in 2024, U.S. large-cap equities and the “Magnificent 7” finally faced headwinds this quarter. The S&P 500 was down 4.3%, the NASDAQ 8.3%. Truthfully, some of this pullback could have been warranted on valuation alone. As we noted in last quarter’s newsletter, leading up to this year, many publicly traded U.S. equities had been trading at valuations wholly untethered from reality— so much so, our investment team wrote a piece for the National Post in February, as part of our newly launched Quiet Investing series, actively warning against the hype. Only now, with the recent pullback, are some of these businesses back into more reasonable valuation territory.

Indeed—and as is so often the case—while the dominant belief structure entering this quarter was one thing (hubris in American exceptionalism), what actually outperformed (Chinese and European equities) was another. Funds flowed outside of the U.S., into these markets, as investors appeared to awaken to the structurally lower valuations.

Looking forward, the key question on everyone’s mind are tariffs. As this letter goes to print, President Trump appears to have blinked (a little) and has granted a reprieve to some of the steepest reciprocal tariffs. A temporary 90-day exception on tariffs for key tech products, including smartphones, laptops and semiconductors, has also been put in place. However, China and the U.S. remain locked in a tense standoff, with both sides signaling a willingness to escalate if negotiations falter.

In truth, no one really knows how far, or how long, this will go on. Here is what we do know: tariffs tend to be inflationary for the countries imposing them. They will undoubtedly create pressure and cause difficulties for companies with international supply chains and customers. Moreover, and more likely than not, the trade war will also weaken economic growth, more or less everywhere it is being imposed. That includes the U.S. and Canada.

This puts the equity investor in an exacting position. On the one hand, no one wants to catch a falling knife. Investor unease right now is based on real economic threats; one anticipates that earnings expectations for many companies will need to come down. On the other, the equity of many fundamentally great businesses is becoming increasingly attractive. In short, this moment calls for bottom-up precision; a scalpel, not a hacksaw.

Amidst the indiscriminate sell-off in Canadian markets, we are seeing some highly compelling opportunities among businesses that are effectively immune to potential tariffs and others that have their own idiosyncratic catalysts / value creation plans. Among U.S. equities, we are starting to see opportunities to acquire high-quality large cap companies that we have always admired at more reasonable valuations, a silver lining amidst the current storm clouds. And we continue to find opportunities to invest in high quality European businesses, which have for some time now traded at valuation levels structurally lower than the U.S.

Fixed Income

Not to be outdone by the chaos in equities, fixed income markets delivered one of their most momentous quarters in recent decades—marked by swelling yields, a bruising selloff in Treasuries, and the first serious questioning of the U.S. dollar’s safe haven status in a generation.

As we warned in our latest for the Financial Post, bond vigilantes—investors who sell off government bonds in response to fiscal policies they perceive as reckless, thereby driving up yields and borrowing costs to enforce discipline—seem to be back. We saw them first this quarter in January, when, in response to the UK budget and spending plans, the UK bond market experienced significant turmoil. The 30-year “gilt” yield surged past 5.38%, reaching its highest level since 1998, while the 10-year yield climbed to 4.82%, levels not seen since 2008.

We saw them next in March, after Germany’s government announced a historic fiscal overhaul, including a €500 billion infrastructure fund and reforms to borrowing rules aimed at increasing defense spending. This marked a significant departure from Germany’s traditionally conservative fiscal policies. The announcement led to a selloff in long-dated German bonds. The 10-year bund yield experienced its largest daily rise since March 2020, and the 30-year yield saw its biggest jump since October 1998.

And lately, we’ve been seeing apprehension in the U.S, as a reaction to President Trump’s trade war. The yield on the 10-year Treasury bond rose to 4.44% on April 14, up from below 4% earlier in the month, marking the largest weekly yield increase in over 20 years. Simultaneously, the U.S. dollar weakened nearly 5% against major currencies in April, despite rising bond yields, suggesting diminished demand for dollar-denominated assets. Former Treasury Secretary Janet Yellen noted that investors seem to be shunning dollar assets, signaling unease about the safety and reliability of U.S. financial instruments.

“I was watching the bond market. It’s very tricky” President Trump recently admitted.

Looking forward, we expect central banks to hold off as long as they can before they start cutting rates. They will face competing challenges from this tariff shock. Tariffs are like a tax—increasing them is like pulling the handbrake on the economy. However, they also directly contribute to headline inflation. So, central banks will have to manage the immediate impact of inflationary pressures, while bracing for potential drops in demand and spending.

Our fixed income funds were defensively positioned entering into this period and remain so today. Credit spreads have been tight for some time, widening out only recently on concerns over growth and the uncertainty in markets. They are not, however, at levels previously seen in past financial crises or recessions, and there remains considerable risk still in credit and fixed income markets overall. Like in equities, therefore, now is an important moment for investors to be highly selective. In our bond funds we are being cautious, while keeping some dry powder ready to be deployed should material buying opportunities emerge.

Alternatives

Our private and alternative investments continue to deliver steady, consistent returns despite the significant volatility and “noise” in the global capital markets.

The Focus Infrastructure Fund had a material positive event in Q4, with the announcement that Alignvest Student Housing REIT would be acquired by Forum Real Estate Income & Impact Fund. As you may recall, one of the key elements of our original investment thesis for ASH was the potential for a smart consolidator to arbitrage the differential between single, one-off property deals and a large, diverse, well-managed portfolio that would be attractive to an organization looking for an easy way to achieve immediate scale in the sector. We expected the buyer to be a large, multinational player like Brookfield, Blackstone or a sovereign wealth fund—but in the end, it was the enterprising group at Forum (which has quickly become one of the top three Canadian players over the past two years). Based on the transaction price and accumulated distributions during our four-year holding period, the annualized return on our investment was in the high teens—a highly successful outcome for Focus clients.

In terms of new developments, we recently made an investment into a high-quality European infrastructure asset: a water utility with an effective monopoly in the Valencia region of Spain.

The Focus Real Estate Fund benefited similarly from the ASH deal, as well as a particularly strong quarter from Hazelview Capital Corporation, which continues to see strong net operating income (NOI) growth at its stabilized properties and had a material uplift in the value of its large development project at 1141 Bloor West. This new mixed-use development will be a master-planned community that includes residential, office, and retail spaces. Along with the buildings, there will be an abundance of community amenities, including a new public road and public park. As the project continues to be de-risked and recapitalized at lower financing costs, we expect further material increases in the carrying value.

Elsewhere, we recently made an allocation to a new partner who is pursuing opportunities in the niche area of ground leases, which offer a compelling (and highly inflation-protected) cash flow stream. We are also in active due diligence on several new investments in senior housing and large bay industrial assets. We are excited about the diverse portfolio of specialized partners we have assembled in real estate, who have demonstrated the ability to grow NOI and add value to the underlying assets, regardless of quarterly fluctuations in interest rates and the fallout from large global institutions—many of whom seem to still be dealing with the difficulties of portfolio rebalancing.

Within the Private Debt Fund, our partners continue to benefit from higher base rates and attractive spreads to generate strong absolute returns. We are mindful of the deteriorating macro environment and the risk of overcapitalization in the private credit industry broadly but are confident in the disciplined risk mitigation of our partners to navigate potential hiccups in the sector. We continue to look for new investments in this area, with a particular focus on asset-backed lending, which would introduce a complementary and differentiated cash flow stream from some of our existing middle-market direct lenders.

The Focus Absolute Return Fund continues to perform as expected, as our partners have proven adept at navigating the tumultuous public markets and finding ways to generate consistent, uncorrelated returns.

Final Thoughts

There’s an old saying that the middle of the storm is not the time to fix your ship. While this period is certainly precarious, we invest the way we do, and have built portfolios the way we have, for moments exactly like this.

Looking forward, we do not know for certain exactly how these large economic forces now at work will settle. We are, however, confident in the companies and leaders in which are invested, as well as the resilient nature of our multi-asset portfolios. Moreover, coming into this period, we had actively avoided the worst of the froth in U.S. equity markets, and had positioned our fixed income funds defensively. So, while we were as bewildered as everyone else by the egregious act of self-harm the Americans committed on April 2nd, we were also not caught, so to speak, flat footed. It is the goal of our investment team to construct portfolios that can deliver regardless of where we are in the economic cycle.

The world economic order appears to be changing. If ever there was a time in recent memory to be active, and not blithely passive, it may be now. A discerning eye is more important than ever.