Do geopolitics matter in investing?

By the time guests arrived at the Four Seasons in Toronto, the temperature had already fallen well below what anyone would describe as reasonable. It was evening, cold and dark; and yet guests had braved a polar vortex to assemble inside. They had come to hear Professor Janice Stein — featured keynote at our recent Quiet Investing event — speak about the state of the world.

Days earlier, at the World Economic Forum in Davos, Canadian Prime Minister Mark Carney had delivered a widely lauded speech on the same topic. Without invoking Donald Trump by name, Carney declared there had been a “rupture” in the old ways: former assumptions about sovereignty, restraint, and cooperation were no longer holding, and the system that markets had learned to price against was being renegotiated in real time.

Much had already happened by this point in the year. In early January, U.S. forces launched strikes across Venezuela, captured President Nicolás Maduro and his wife Cilia Flores, and flew them to the United States to face federal criminal charges. Around the same time, President Trump intensified pressure on Greenland’s future, threatening tariffs and refusing to rule out military intervention. This was an unprecedented, widely decried departure from norms and the post-Cold War order, directly pitting America against her sworn NATO allies.

To say nothing of the raging fires, messes and tensions in Iran, Ukraine or Taiwan.

And so, the room was packed that evening for an open, engaging discussion on Canada, geopolitics and the future of the world. The audience engaged in a spirited Q&A, and left with many insights from Professor Stein, a small parting gift of maple syrup, and much to think about.

Including, naturally, these questions:

Do geopolitics matter within investing?

If so, how and when?

And:

How does one position oneself amid all this geopolitical upheaval?

First, principles

Geopolitics is the study of how physical geography, natural resources and, increasingly, technological and economic factors shape international relations, foreign policy and the balance of power between nations. It examines strategic competition for control over territories, resources and influence.

Clearly, geopolitics matter to citizens concerned with the wellbeing of their societies and that of future generations. For instance, if you care about democracy, it makes sense to pay attention to what’s happening right now worldwide. But how much geopolitics matter for investing in financial assets is a more nuanced question.

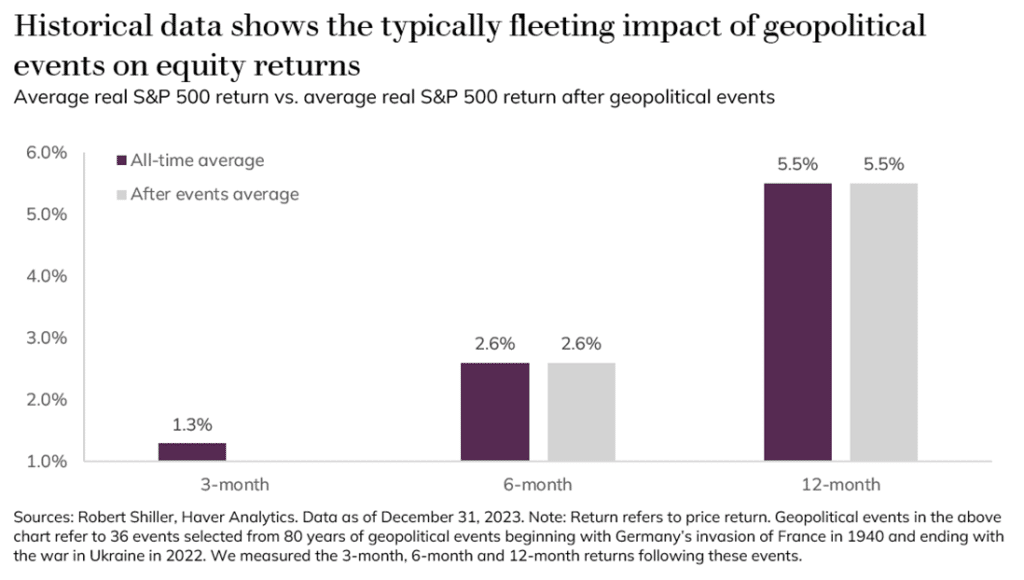

In fact, one widely cited JP Morgan study—which examined major geopolitical events from Germany’s invasion of France in 1940 through Russia’s invasion of Ukraine in 2022—found that, while equity markets tend to underperform in the immediate aftermath (three months), returns over six and twelve months are effectively indistinguishable from periods without such events. The report notes “when you consider the average equity investor experience, it’s as though the event never happened.”

In our experience, geopolitics is not, on its own, the make-or-break factor for successful investing. While an informed view of the global context is important, geopolitics is only one of many inputs investors must consider, and not the most important one.

This is true despite how loud headlines can be

Let’s begin with some first principles. Even though it’s common to speak this way, it is not possible to invest in a “market,” a “country,” or even a “theme.” When we say we are investing “in Canada,” for instance, we really mean we are buying individual financial assets — equities, bonds or otherwise — that happen to be traded in Canada. Those individual assets are driven by distinct forces, some micro and some macro.

Micro forces are company-specific factors that drive a business’s inherent worth. The main forces here are management, competitive position, business model, industry dynamics, and capital allocation. Investors, like Warren Buffet, who concentrate first and foremost on micro forces are considered “bottom-up investors.”

Macro forces relate to broader economic and financial conditions, such as interest rates, inflation, fiscal policy or GDP growth. Investors, like George Soros, who famously broke the bank of England, who concentrate on macro forces, are considered “top down” or “macro” investors.

For example, if you purchase Shopify stock, it will be influenced by the number of merchants joining and remaining on its platform, the growth in gross merchandise volume flowing through those stores, the adoption of higher-margin services such as payments and capital, and the company’s ability to scale internationally while improving operating efficiency. These are primarily micro forces.

If you purchase stock of a Canadian bank, it will be influenced by loan growth — particularly residential mortgages and commercial lending — net interest margins, credit quality and loan loss provisions, as well as fee income from wealth management and capital markets divisions. The health of the housing market, employment levels and the shape of the yield curve will all affect earnings, as will the regulatory environment. These are mostly macro forces (banks are strongly exposed to the overall economy).

Both companies would be greatly influenced by how leadership runs them.

Importantly, geopolitics impact macro conditions. And they are worth paying attention to when they change the rules of the game. However, this depth of impact is rare; and much more common at an industry or singular sovereign nation level than the “market” at large.

A trade war, a hot war, an oil price shock, or a technology embargo, for instance, can materially alter the cost structure of an industry or a company’s revenue potential. When the United States restricted the export of advanced semiconductor chips to China, companies such as NVIDIA, whose high-performance GPUs are critical for artificial intelligence and data centers, were forced to rethink sales strategies and geographic exposure. Conversely, when China shifted from Maoist central planning to market-oriented reforms in the late 1970s and opened itself to foreign investment, it unleashed decades of capital inflows, productivity growth and corporate expansion. These were structural shifts and markets responded accordingly.

Geopolitics can also matter insofar as they affect investor confidence, particularly foreign capital. When a country’s leaders or policies move too far outside what markets consider predictable or institutionally sound, investors demand compensation for that uncertainty. Argentina is a clear example of this: after repeated sovereign defaults, episodes of hyperinflation and capital controls over the past century, investors require significantly higher yields to hold its government bonds. Capital, quite rationally, demands payment for bearing uncertainty.

A lot of noise

Often, however, while political headlines are loud and absorbing, they do not change the underlying structure of the game.

A substantial body of research shows that major geopolitical or political events may influence markets in the short term but they do not consistently predict long-term returns.

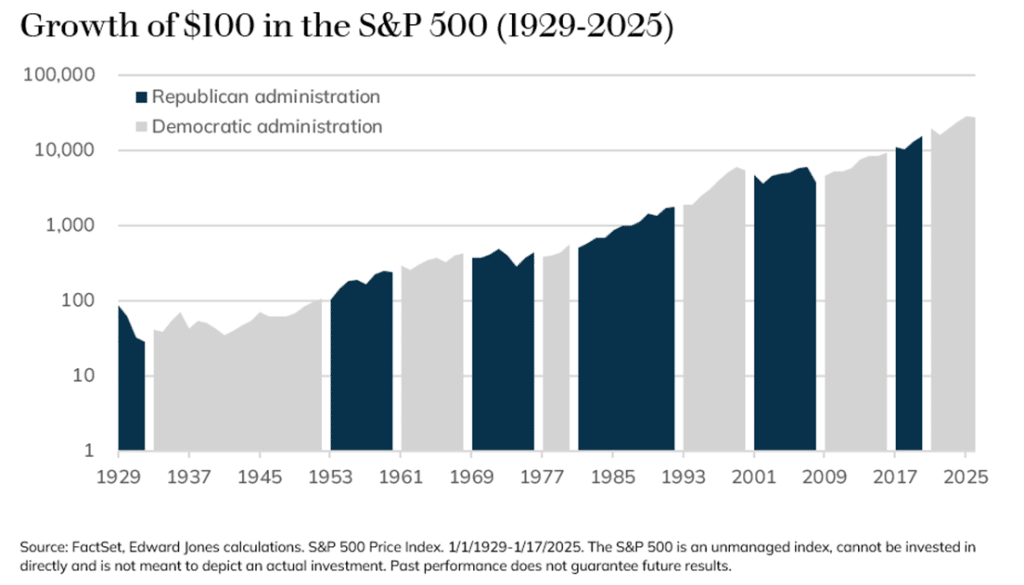

For example, long-term analysis of nearly 100 years of U.S. presidential terms shows that the broad trend of stock market returns (as measured by the S&P 500) has marched upward regardless of which Presidential administration was in office.

Elections themselves are only one of many inputs to market performance rather than a dominant driver.

Moreover, research on geopolitical risk shows that equity markets tend to react negatively to spikes in geopolitical risk measures in the short term, often reflecting increased volatility or flight to safe assets, but the long-term impact on returns is usually modest. Historical data indicates that while events such as wars or political crises can coincide with near-term market turbulence, markets tend to absorb these shocks over time and “normalize” when fundamentals reassert themselves.

These findings support the idea that geopolitics matters when they change the rules of the game, but day-to-day headline noise alone is usually just that. Noise.

The geopolitics of this moment (and what to do about it)

This brings us to the present moment, where the current U.S. administration has disrupted long-standing assumptions about trade, alliances and government intervention in capital markets.

Donald Trump is an outlier president. He is the extreme case. Likewise, many of his proposed geopolitical and economic positions have been extreme: he has shown hostility to the Federal Reserve, floated aggressive sweeping tariffs, threatened allies, and signaled a willingness to use trade policy and military force as blunt instruments. Had many of his policies been fully implemented, the economic consequences would have been significant.

But markets have learned to discount much of his rhetoric, because, to use an acronym that has entered investing lexicon, Trump also usually TACOs (“Trump Always Chickens Out”). If you had pulled your money out of equity markets in April 2025, at the height of the “Liberation Day” tariff episode, you would have missed a sharp double-digit rebound in global equities in the months that followed.

That said, there are areas where his actions have had real effects.

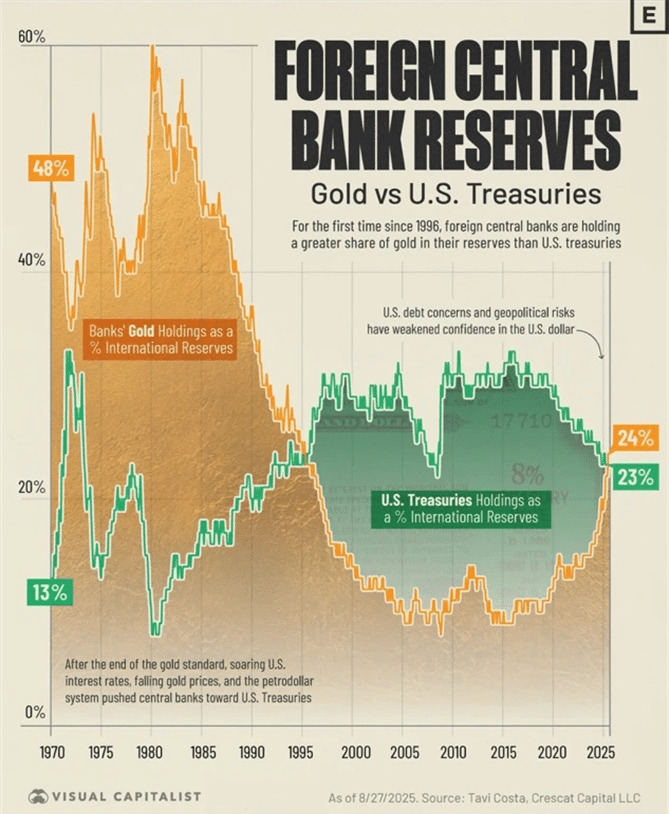

By antagonizing allies and unsettling institutional investors, President Trump has engineered a worldwide “sell America trade at the margin” trade. Clearly, (practically) everyone still owns some U.S. financial assets. But some central banks and large institutions reduced their Treasury holdings at the margin in 2025, including the People’s Bank of China and the Reserve Bank of India.

Currently, global central bank gold holdings now exceed their holdings of U.S. assets. The U.S. dollar’s share of global foreign exchange reserves has fallen toward its lowest level since the mid-1990s. Although the magnitude can be debated, clearly something is going on.

Trump policies have also forced countries to rethink trade relationships. This has obviously been felt most keenly here, at home, in Canada. In so publicly rebuking American bullying, Prime Minister Carney must look for other partnership options. Currently Canada is making a deliberate push into deeper partnerships with Japan, South Korea, India and Mexico, among others.

Further, in bombing Iran, the United States has carried out one of the most significant military escalations in decades, launching coordinated strikes across hundreds of targets tied to Iran’s military and nuclear infrastructure. The campaign has already triggered retaliation across the region, disrupted shipping through the Strait of Hormuz (through which roughly one-fifth of global oil flows), and introduced renewed volatility into global energy and equity markets. Brent crude oil is now up more than 50 per cent since the war began.

The war has also stoked some uncertainty around inflation, to the point that the Federal Reserve recently held off on lowering rates, despite previous pressure from the White House. “We just don’t know what the effects of this will be and really no one does,” Federal Reserve chairman Jerome Powell said, noting that any future cuts would depend on whether inflation continues to fall.

So, what, if anything, does an investor do about this?

First, in our investment team, we sometimes say that macro is defense and micro is offense. In the long run, we believe it is far easier to repeatably put the investment odds in one’s favor with excellent bottom-up analysis, than it is to try to speculate on where asset prices are going due to macro factors. We pay attention to macro conditions primarily for risk management.

Second, this is why diversification matters.

Diversification across asset classes, sectors, currencies and regions reduces dependence on any one political outcome. It acknowledges that the future is uncertain, and better positions investors to win across whatever scenarios unfold. Although investors seemed to have eschewed diversification in 2025, if anything, what we are living through serves as an important reminder that it is as important as ever.

Finally—it’s worth noting that markets always face some manner of chaos. Markets have endured world wars, oil embargoes, sovereign defaults, financial crises and pandemics. Yet through all of it, always, there have been well-chosen businesses who continue to innovate, generate cash flow and reward discerning owners.

The disciplined investor stays aware of world news, and makes adjustments when necessary. History would suggest that, most of the time, it’s not.