The Quarterly Focus – Q3 2025

Good Time Charlie Buys the Stock Market

Global financial markets surged through the third quarter, fueled by looser monetary expectations, resilient corporate earnings, and an unmistakably “risk-on” tone. U.S. equity benchmarks notched new all-time highs, while global indices advanced broadly, with emerging markets leading developed peers amid a weaker U.S. dollar and revived capital inflows. In fixed income, corporate bond spreads tightened toward multi-decade lows, signaling investors’ near-total comfort with risk. For now, markets appear content to ignore nagging concerns over government debt loads, trade and policy uncertainty, geopolitical strain, and historically elevated valuations—choosing, instead, to keep the party going.

There are two key takeaways for clients at this juncture. First—Focus portfolios have delivered strong results year to date, a noteworthy strength given the caution we are taking to avoid the speculative areas of the market (and which have run up the most). Year to date, our diversified mandate, the Focus Fund, is up 9.9% before fees.

The second takeaway relates to deeper questions of where we are now, what risk is, and what intellectual humility and prudence might mean in this moment for investors. If we are not yet at an inflection point, we may be approaching one.

It may be time to pause and ask harder questions.

This Time Is Different — Or Is It?

In 1625, English philosopher Francis Bacon’s collection Apophthegms, New and Old, was published posthumously, in which he wrote: “A prudent question is one half of wisdom.”

It’s a pithy maxim, reflecting Bacon’s broader philosophy that knowledge begins with questioning; that selecting the right questions is at least as important as finding right answers. To that end, and with the spirit of a dead English philosopher in mind, we ask the following:

With everything we’ve seen in this bull market, what signs do we have that this time really is different? Or, are we, as investors, once again falling into a predictable cycle of hype?

Put differently and directly:

How much of your net worth do you really want exposed to companies trading at valuations that have almost never, across the entire history of the stock market, ended well for investors?

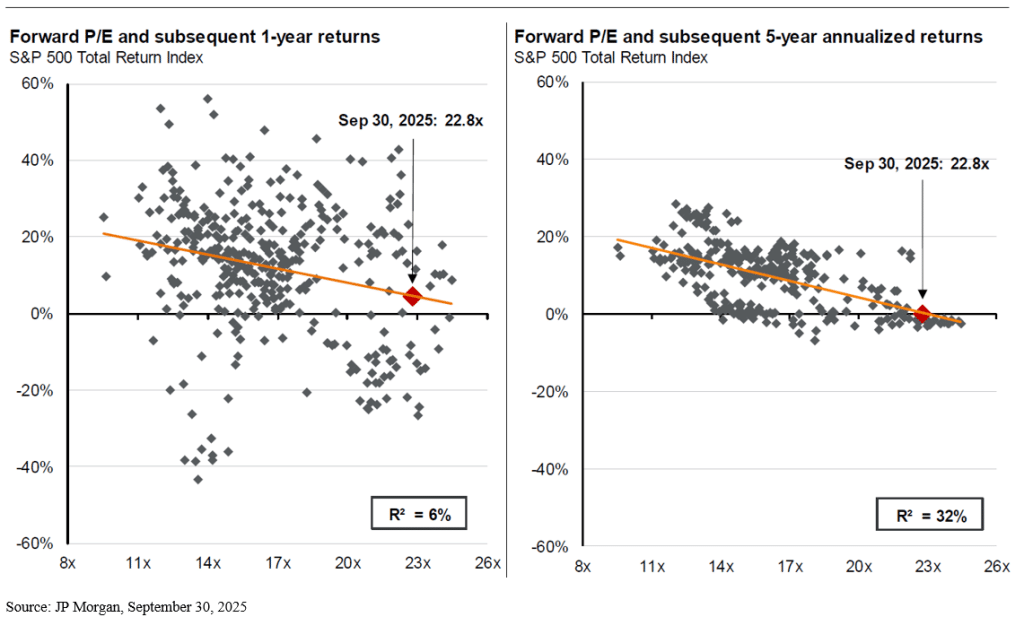

Let’s review some of the facts. The forward multiple of S&P 500 Index is now at ~23x earnings, not quite as high as the 25x from the dot-com era of 1999/2000, but getting there. Historically, such levels have preceded periods of muted future returns. According to J.P. Morgan Asset Management data spanning 1993 to 2025, when valuations have hovered above 21x forward earnings, the S&P 500 Index’s subsequent 5-year annualized real return has averaged in the low single digits, compared with over 7% when starting from more moderate multiples.

Moreover, not only is this index now at its highest level ever, it is also at one of its most concentrated ever. The top 10 stocks make up nearly 40% of the S&P 500’s market capitalization, a level of concentration not seen since the 1950s and greater than the peak of the dot-com bubble. Historically, periods of comparable concentration have tended to precede weaker relative returns for the market’s largest constituents. As leadership narrows, future gains become harder to sustain.

For instance, after the Nifty Fifty era of the early 1970s, the top-ten stocks underperformed the broader S&P 500 Index over the following decade; a similar pattern emerged after 2000, when the largest names fell while the equal-weighted index recovered far faster. In other words, extreme concentration has rarely marked the beginning of durable outperformance. More often, it signals that much of the easy money has already been made.

Naturally, this begs the question: is this time different? And if so, by how much?

The case for the bulls

It’s worth acknowledging there are real reasons for the current bullish reality. The bull case is simple: corporate earnings and economic growth have proven more resilient than expected, today’s best businesses are fantastic businesses, and AI is almost undeniably going to change the world.

To start, at the core of the modern economy are a handful of technology companies which have reshaped the world in their image. These great companies, maybe some of the greatest ever, are behemoth, often quasi-monopolistic enterprises with historically exceptional returns on invested capital, dominant competitive positions, powerful moats, and long records of growth. They command global networks of users, massive data advantages, and a scale of innovation that allows them to compound earnings year after year. That these businesses should trade at valuations above historical averages makes sense: they are fundamentally more profitable, more dominant and (potentially) less cyclical than the corporate leaders of prior eras.

Moreover, all of these firms are deeply exposed to artificial intelligence. Now, whether AI ultimately proves as transformative as the Industrial Revolution, the rise of computing, or the advent of the Internet remains to be seen. But the probability that it will be one of the great technological revolutions of our lifetimes seems high.

The largest public companies are not merely beneficiaries of this shift, they are the architects of it. They are investing hundreds of billions of dollars annually into AI infrastructure, semiconductors, and model development, creating a self-reinforcing ecosystem that could not only expand their economic moats, but accelerate productivity across industries.

On top of all this is the reality that advanced market economies, especially the United States, have digested tariffs and policy uncertainty better than expected (so far, at least) while monetary conditions appear to be easing. In September, the Federal Reserve reduced its benchmark rate by 25 bps for the first time since 2024; more rate cuts are anticipated before end of year, while other advanced market economies are also easing. Cheaper interest rates can belie economic challenges ahead, but they still tend to support the stock market. Low rates are the juice that keeps the party going.

In short, there are genuine reasons for market strength right now, as in every bull market. And, as with every major technological innovation, the world is likely going to look different because of AI.

The question here, however, is not whether this time is different (it obviously is), but by how much and whether what’s happening now is different enough. Can the current momentum of AI overcome the forces of investment gravity—valuation, the hype cycle—in a way never done before?

Or are we simply heading towards a reckoning?

Signs of late-cycle exuberance

The other side of the argument is also simple: no matter if fundamentals were initially sound, valuations have gotten so lofty that all but the rosiest assumptions could now justify them. There are also many worrisome signs of late cycle excess.

As noted above, valuations within stock markets appear stretched and increasingly hard to wrap ones’ head around (this also goes for credit spreads). This is not only true for the mega cap technology stocks like Nvidia, which trades at over 29x next year’s earnings, or Apple, which commands a 31x multiple, but also for many non-tech large cap companies. Even traditionally “defensive” sectors look expensive: Consumer Staples trade around ~21× forward earnings and Utilities near ~19×, both above their long-run norms and hardly bargains for slow-growth businesses.

Paying premium multiples for sectors with slower growth has not been a recipe that has historically rewarded investors.

There is also the critical question here of whether or not the current AI capex boom is as unassailable as is assumed. On the one hand, AI does appear to be an arms race, where some winner-take-all features are present. This implies that the companies pursuing this technology will need to invest truly gargantuan amounts of capital, as fast as possible, to win the game. In theory, this should support continuous capital expenditure into AI.

On the other hand, history warns us that breakthrough technologies tend to overshoot in the near term before they eventually live up to their promise. When railway mania swept through England in the 1840s, or when the dot-com boom fueled excitement over the possibilities of the Internet in the 1990s, there was an initial overbuild in underlying technological infrastructure because of the hype and influx of capital it generated. These massive overbuilds ultimately became productive—the promise of railroads and the Internet was realized—but only after a painful reset in which exuberant forecasts met the reality of cash flows, companies failed, and significant capital was impaired. The NASDAQ Composite Index, for instance, declined almost 80% from March 2000 to October 2002. In a typical technology hype cycle, hype is both catalyst and cost: it mobilizes the capital that builds essential infrastructure, yet in the short term, it also misallocates capital into projects that can’t earn their keep.

In this case, two of the largest AI spenders still rely heavily on advertising in their core business, and advertising tends to be cyclical (even if online ad share has a structural tailwind). Meta has guided $60 B–$65 B for 2025 AI infrastructure and data center capex, and has discussed even higher ranges in subsequent commentary; yet it still generates substantially all of its revenue from advertising. Alphabet likewise lifted 2025 capex to about $85 B and, even with strong Cloud growth, its search and YouTube ad businesses remain the largest revenue lines. If ad growth cools, the near-term cash flows underwriting this AI build-out look less bulletproof than bullish narratives imply.

What makes these investment levels more concerning is the creep of vendor financing and backstop structures that can blur organic demand. We saw this movie in the last telecom boom: vendors financed customers’ purchases, juicing reported sales; when the cycle turned, Winstar went bankrupt and Lucentfaced costly litigation over such arrangements. Nortel, the Canadian telecom-equipment giant that overexpanded into the late-1990s boom, also used aggressive practices like vendor financing; they too got hit by the 2001 telecom bust, then unraveled amid major accounting restatements, ultimately filing for bankruptcy in 2009 and liquidating its businesses.

Today’s AI infrastructure rush is, as they say, not repeating but rhyming. CoreWeave, a specialized GPU cloud company, has layered large debt facilities and entered a $6.3 B agreement under which Nvidia will buy any residual unsold capacity through April 2032; CoreWeave also required waivers after breaching terms on a $7.6 B loan last year. Meanwhile, GPU-backed lending is spreading: Lambda secured a $500 M loan with Nvidia chips as collateral, part of an emerging market for GPU-collateralized debt. These structures can sustain momentum, but they also distort the demand signal and intertwine supplier balance sheets with customer utilization, leaving the build-out vulnerable if end-markets under-deliver.

On top of these arrangements are classic late-cycle tells. Retail speculation is roaring. Leverage is also elevated, with FINRA margin debt hitting a record ~$1.13 T in September. And then there are the companies raising capital to buy bitcoin (BTC) rather than to fund productive investment: this year MicroStrategy sold$2.0 B of 0% convertible debt to explicitly acquire more BTC, Semler Scientific issued convertible notes and equity to purchase BTC through 2025, and Tokyo-listed Metaplanethas pursued bond and equity raises to expand a bitcoin treasury strategy on a massive scale. Taken together, these are hallmarks of exuberance rather than discipline.

Meanwhile, in the bond market, corporate credit spreads, too, are compressed at very low levels.

Do these red flags mean everything is bad out there in stock market? No, of course not. There remain many good companies to invest in, which are doing something productive with their capital, which are not priced for perfection. We continue to find and invest in these businesses, and their compounding serves our client portfolios. But these signs do paint a picture of complacency to risk. Investors would be remiss not to note and guard against these extremes and their normalization.

Positioning

What are we doing in this environment to advance portfolios while also safeguarding capital? As always, we hew to timeless investment principles, including requiring the valuation of our holdings to be at least tethered to reality. We are aware of the larger macro risks playing out currently and are being cautious not to expose our clients to scenarios where everything must go perfectly to register a modest return. As bottom-up investors, we aim to score points in the micro, while avoiding loss in the macro. This is what we have always done and will continue to do.

Within public equities, we continue to find opportunity in under-followed small and mid-cap companies, where information edges and multi-year growth runways can still be bought at reasonable valuations. There are structural advantages in this area—less sell-side coverage, more idiosyncratic drivers, and the ability to grow—which remain true despite the way so many large cap stocks trade. We say this almost every quarter and it continues to be the case.

Opportunity also remains better outside of the U.S. Indeed, it has been a good year so far for international equities: the Focus International Equity strategy is upover 30% year-to-date.

While much of this quarter’s letter has concentrated on the stock market, so much of the “risk-on” tone also extends to the corporate bond world, or credit. Like with equities, our stance is deliberate and selective.

Lastly, private and alternative assets continue to act as a ballast in the multi-asset portfolios. Volatility in public markets has only sharpened their appeal. Real estate, private credit, and infrastructure investments are delivering steady, contractual cash flows. We maintain exposure to them because we believe they contribute to true diversification.

Final thoughts

In 1967, Danny O’Keefe wrote Good Time Charlie’s Got the Blues, a ballad perhaps not as erudite on its surface as Bacon’s Apophthegms but, in its own way, philosophical. Riding on fingerpicked acoustic guitar and a spare, country-folk arrangement, O’Keefe sings the lament of Charlie, a man who’s chased the good times so long he’s left with an existential hangover. His friends have moved on, the party’s over, and a discomforting quiet follows him, exposing the cost of his carefree, careless life.

Obviously, financial markets do not have the blues right now; rather the opposite is true. Almost nothing seems to dampen the spirits of the retail investor! Good Time Charlie is buying the stock market.

Historically, however, malaise tends to follow exuberance, if not an actual reckoning. Especially the longer expectations float away from reality, the less attractive future returns for those asset classes become. And the more painful the consequence. Moreover, as much as it’s possible for this party to last a good while longer, we should not ignore what late cycle signs have emerged.

To this point, Bank of America strategists published a report this summer arguing that 19 out of 20 valuation metrics appear expensive based on historical data. They went on to argue these premiums were warranted by “compositional changes of the benchmark” adding “earnings visibility has improved with healthier balance sheets and corporates pivoting from low-quality growth from free capital/ global cost arbitrage to efficiency.”

Frankly, we don’t know whether these strategists are right or wrong. We won’t be able to know for some time, because this is the nature of valuation, an important but epistemologically precarious and subjective concept, which can only truly be reflected upon in the rear-view. But— and just asking the question—in how many instances historically have similar things been said right before the rug was pulled from under the market? How has such thinking served investors?

Traditionally, when the market gets complacent like this, investors should take greater caution. The next great trade may simply be restraint.