The Quarterly Focus – Q2 2025

What Lurks Beneath

Markets opened this quarter on shaky ground. On April 2nd—what now feels like a lifetime ago—U.S. President Donald Trump announced sweeping reciprocal tariffs, a dramatic escalation from first-quarter rhetoric and the most protectionist agenda in over a century. The move sent shockwaves through public equity and bond markets, drawing retaliatory measures from China, disrupting supply chains, pausing business investment, and fracturing decades-old global trading alliances.

In the weeks that followed, the administration walked back its most aggressive threats, offering temporary exemptions to some countries and delaying implementation for others. Still, and despite trade deals made with London and Beijing, significant levies remain in place, particularly on aluminum, car-related parts, and the 10% universal import tax.

“I may do it. I may not,” Trump recently told reporters. “I mean, nobody knows what I’m going to do.” These words, spoken about Iran, might just as easily have applied to any area of U.S. economic policy, so surreal has American geopolitical theatre become.

Now, as the third quarter begins, the world remains in a kind of limbo. Equity markets have largely recouped their tariff tantrum losses: year to date the S&P 500 Index is up 5.5% in local currency (and down 0.2% in CAD), while the S&P/TSX Composite Index has climbed 8.6%. Bond markets, too, appear momentarily assuaged: after spiking to 4.6% in May over concerns about unchecked spending and the fiscal impact of the “Big, Beautiful Bill” making its way through Congress, the 10-year Treasury yield hovers just under 4.3%.

In short, a peculiar calm has settled across global markets, though it’s a calm born less of resolution than of temporary reprieve. When, and how much, will economies feel the impact of tariffs? What will be included in Trump’s signature tax bill? Will wars in the Middle East de-escalate or expand? Many of the most critical questions remain unanswered.

Against this backdrop, there is both good news and bad. The good news for Focus Wealth Management clients is a story of resilience. Despite this year’s volatility, portfolios have held up well and performed as designed. The conservatively positioned Focus Fund, for example, is up almost 7% year to date. That stability is no accident; it reflects the disciplined investment philosophy we apply in all conditions, a few things going our way, and the structure of our multi-asset portfolios.

The bad news: not all calm signals peace. In key areas—trade, fiscal policy, and global conflict—tensions continue to simmer just below the surface. The potential for dislocation remains. In many parts of the equity market, valuations do not appear to compensate for underlying risks, as some areas trade as untethered from fundamentals as they were at the prior February peak.

Investors are right to be wary of these waters. Vigilance remains essential.

Half-Year Check-In

With summer finally here and half the year gone, how have client portfolios, and our firm, performed year to date?

In a word: well. While external headlines have been defined by disruption and geopolitical ambiguity, our portfolios, and the broader progress of the firm, tell a quieter, steadier story.

Focus portfolios have delivered excellent results through this period, compounding client wealth despite more turbulent market conditions. Diversified equity and fixed income portfolios are solidly in the green and ahead of their respective benchmarks. The Focus International Equity Fund, for example, is up over 20% this year. Meanwhile, the alternative funds continue to proceed along on their expected paths, with scant correlation to public markets. All funds continue to deliver strong results over longer time horizons.

Beyond investment performance, we remain relentless in our pursuit of excellence and the value we deliver to clients. That commitment is reflected in recent strategic additions to our investment team and governance.

We are pleased to welcome Alexander MacDonald, CFA, to the role of Portfolio Manager. A seasoned investor and licensed professional engineer (P.Eng.), Alex was previously a portfolio manager at Davis Rea, where he managed North American large-cap equities. His prior experience includes roles in equity research at Cowan Asset Management, National Bank Financial, and Wellington West.

We also welcome Kara Lilly, CFA, as Senior Investment Strategist. Formerly a Partner at Mawer Investment Management, Kara brings deep expertise in global equities and capital allocation, having served on multiple award-winning funds. She played a key role in building Mawer into one of Canada’s most respected asset managers, and her investment commentary has been featured in the CBC, The National Post, and The Globe and Mail.

In parallel, we’re proud to welcome four exceptional leaders to our Advisory Board:

•Ira Gluskin – Esteemed Canadian investor and co-founder of Gluskin Sheff + Associates

•Clare Sellers – Accomplished investment professional and governance expert

•Kenneth Irving – Executive with a legacy of long-term value creation across energy, industrial, and digital sectors

•Mary Abbott – Chief Legal Officer at the Healthcare of Ontario Pension Plan, with deep experience advising pension plans and private equity sponsors

These appointments reflect our ongoing commitment to building a firm of enduring quality—one that continues to evolve in service of our clients’ long-term success.

Outlook

In 1975, Steven Spielberg and Universal Pictures released a film that would change cinema forever. Jaws wasn’t just the first summer blockbuster. It was a study in tension. For much of the film, the danger remains unseen. It’s not the shark you fear—it’s the stillness. The silence. The feeling that something is there, just out of sight.

We, the audience, watch with knowing as swimmers enter the water onscreen, unaware of the dangers below.

Is this the environment we find ourselves in now? Markets look calm. Headlines are quieter. Retail investors appear to be buying the stock market. But beneath that surface, risks remain: economic fractures, stretched valuations, and fiscal foundations beginning to buckle.

Looking forward, critical geopolitical and economic questions are anything but resolved.

Monetary Environment

Central banks, for their part, are treading cautiously. The Bank of Canada held its policy rate steady at 2.75% this quarter, pausing after a 225-basis-point easing cycle. With inflation cooling to 1.7% in May, the door remains open to further cuts, particularly if tariffs begin to drag on growth. In Europe, the ECB and several Nordic central banks cut rates to support fragile economies. The Bank of England, by contrast, held firm, citing persistent wage pressures.

The U.S. faces a more fractured policy landscape. While the Federal Reserve left rates unchanged, its members remain split. Some are pushing for cuts as early as July. Others warn that tariffs and immigration policies may prove structurally inflationary. Further complicating matters is the continued erosion of central bank independence, with the U.S. president applying direct pressure on Fed decision-making.

Like other market observers, central banks seem to be waiting for the other shoe to drop, charting as steady a course as possible in anticipation.

The Future of the U.S. Dollar

Zooming out, one of the more pressing questions is the role of the U.S. in the global economic order. America’s inward turn, intensified on Liberation Day, has frayed alliances and weakened the structures that underpinned decades of economic leadership.

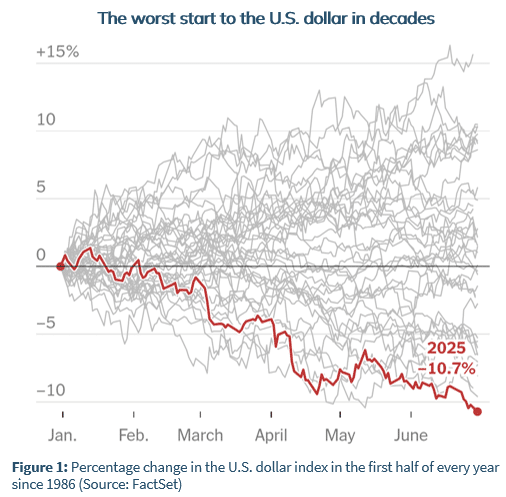

The U.S. dollar has fallen over 10% against major currencies this year, while the yield on treasuries has remained elevated, a sign of eroding trust and strained trade relationships (see Figure 1). That’s troubling. The U.S. has long benefited from its status as the world’s reserve currency, enabling fiscal deficits few other countries could sustain while still accessing cheap debt.

One would think the administration would want to protect that role. Instead, its actions have increasingly called it into question.

Of course, the U.S. dollar isn’t about to lose reserve status overnight. It is deeply embedded in the global system, and no viable alternative exists today. Even if a transition were underway, which is not a foregone conclusion, it would take years.

Still, the mere act of jeopardizing that status is reckless. U.S. government debt to GDP is at its highest level since World War II. If the “Big Beautiful Bill” passes, it may surpass it. Interest payments now exceed annual military spending, and the U.S. lost its remaining AAA credit rating from Moody’s this past quarter. In short: at a time when international appetite for U.S. debt is waning, America needs cheap capital more than ever.

Perhaps the administration will navigate this moment without reigniting bond market volatility. We should all hope for this outcome. But we also wouldn’t count on it.

Canada

By contrast, one country appears to be turning a corner: Canada.

While the White House has ignored fiscal prudence, there are signs of more rational policymaking at home. Canada is finally showing evidence of economic leadership.

March’s rollback of the consumer carbon tax marked the beginning of a broader shift. Over the second quarter, Ottawa moved forward on efforts to lower interprovincial trade barriers, invest in housing, and streamline permitting for key infrastructure. These are small steps, but they’re meaningful and in the right direction.

We’re still in the early days. But as the saying goes: tough times make tough people. For the first time in a while, Canadian leadership feels more aligned in its aim to attract capital, build great companies, and encourage productive investment.

Asset Outlook

From an investment perspective, the simplest way to describe our stance is this: we like what we own, and we’re skeptical of much else.

Our portfolios continue to be comprised of companies and leaders we believe in, and are constructed in a way that we believe can advance client wealth in spite of whatever “the market” is doing.

Our view on broad market indices like the S&P 500 is decidedly less enthused. While we continue to find selective opportunities in both equities and fixed income, we are often struck by the mental gymnastics required to justify current valuations.

In equities, we remain cautiously constructive, and highly selective. The forward P/E on the S&P 500 sits around 22x, well above the historical 16–17x average. AI enthusiasm and U.S. mega-cap dominance continue to drive sentiment. While the market moves higher, however, fewer and fewer companies participate in the gains. According to the Bank of America, of the 503 stocks in the S&P 500, only 22 have recently reached historical highs, suggesting that the rally is a narrow one. The gap between the best and worst performers is getting wider.

Opportunities do remain. Developed Asia and parts of Europe and the UK are attractively valued and under-owned. Small and mid-cap U.S. names—largely ignored in the AI rush—still look compelling. We also find some value, at the margin, in real-economy cyclicals such as Canadian financials.

In credit, our message remains the same: be discerning. Yields on investment-grade credit are neither unattractive nor the deal of a lifetime. We remain focused on higher-quality issuers with manageable refinancing needs.

Lastly, private and alternative assets continue to act as a ballast in the multi-asset portfolios. Volatility in public markets has only sharpened their appeal. Real estate, private credit, and infrastructure investments are delivering steady, contractual cash flows. We maintain exposure to them because we believe they contribute to true diversification.

Final Thoughts

So far, 2025 has been a constructive year for client portfolios and a more precarious one for the world at large.

That disconnect may feel disorienting, but it’s not uncommon. Investors often assume that strong macro conditions lead to strong returns, and weak ones to poor performance. But great investing doesn’t require a perfect backdrop, nor does it depend on predicting the macro environment. It’s also possible to compound wealth even if the sitting U.S. president never makes up his mind—though admittedly, this would help.

After a chaotic start to the quarter, much of the volatility has mercifully subsided, just in time for everyone to head to cottages and lake country. The calm has been a welcome reprieve, if somewhat unnerving.

As in the eponymous film that inspired this quarter’s theme, in investing, it pays to look beneath the surface. The smart move is never to panic. It’s to pay attention. To prepare. To recognize that “calm” waters don’t guarantee safe passage.

And yes—to make sure you’re in the right boat.