The Quarterly Focus – Q4 2024

The following is an excerpt from the quarterly newsletter distributed to clients.

Q4 2024 – America, America

Rules for riding a tidal wave

The year 2024 proved to be a constructive year for investors. Despite momentary jitters in August and late December, overall market sentiment remained firmly optimistic. Several factors fueled the enthusiasm: the global economy is now widely expected to achieve a soft landing, U.S. election results were conclusive, inflation fears dissipated, central banks began cutting benchmark rates, and China ramped up its economic stimulus. Against this backdrop, the S&P 500 soared by 25% in local currency terms, while the S&P/TSX Composite Index followed closely with a 22% gain.

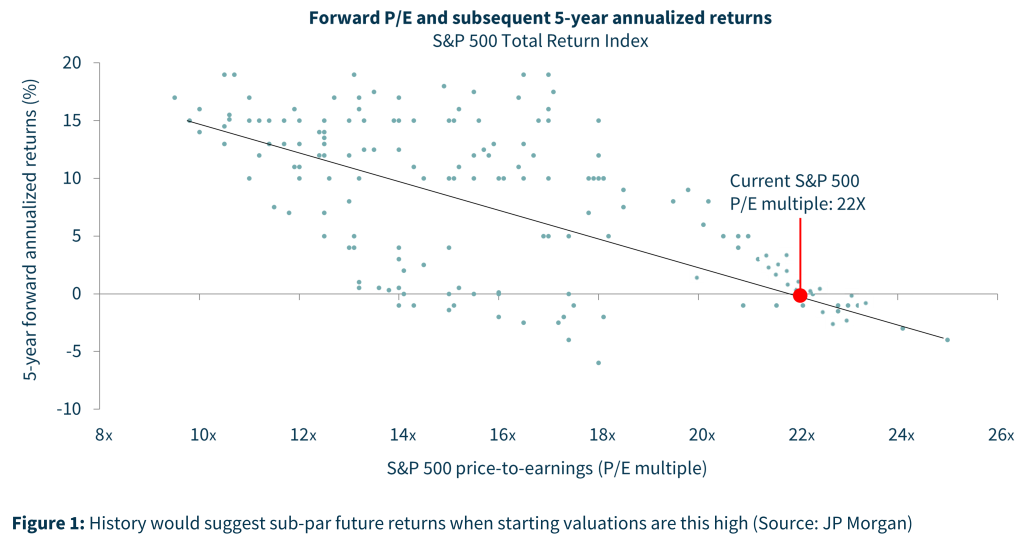

American exceptionalism and the so-called “Magnificent 7” – Apple, Microsoft, Alphabet (parent of Google), Amazon, Nvidia, Meta and Tesla – were by far the biggest drivers behind this stellar performance, accounting for 50% of the year’s return. The belief that American companies are the best in the world (justifying lofty valuations), will continue to be the best in the world, and the American economy is most resilient has rapidly become an unassailable truth held among many market participants. Add to this expectations of the new, pro-business administration, and few now bet against America – at least in equity and currency markets. Over the year the USD was up strongly against a basket of major currencies. American public equities now represent 70% of the global market capitalization, up from 30% only years ago. Valuations for many large-cap U.S. equities are now the richest they’ve been since the tech boom of the late 90s (we all know how that period ended). As Figure 1 illustrates, history would suggest sub-par S&P 500 returns when starting valuations are this high.

As ever, when everyone agrees in investing is usually when either risk or opportunity is brewing. Right now, markets are full with risk-on attitude and hype. Froth is back. This is especially apparent in U.S. equities—many of which trade significantly above historical averages and at valuations untethered from reasonable growth expectation—as well as increasingly tight credit spreads. Of course, there are concerns that could potentially douse cold water on this enthusiasm: investors worry over trade wars, geopolitical risk and what President Trump will or will not be able to do. Nonetheless, the hype could surprise investors with how long it lasts.

In this environment, the Focus team continues to find attractive investment opportunities within public equities, fixed income, and alternatives—and chart a steady path forward. We remain disciplined in our approach, investing in fixed income and equity where the odds are in our favour, where both near and longer-term return potential, as well as valuations, are compelling. We encourage clients and friends to eschew the hype, stay focused on strategies that compound wealth over decades not quarters, and continue to require sound investment cases, even as others abandon theirs. Although the hype pervading certain areas of markets could persist, history would suggest now is the time to prepare for when the tide does eventually— inevitably—turn.

Extremes, America and investment case discipline

Like the gravitational pull causing tides in the ocean, belief structures are essential forces in markets. When everyone believes the same thing is typically how you know the tide is close to an extreme of all-the-way-in or all-the-way-out, and when it’s most important to watch how one is positioned. Right now, the tide has come rather far inshore with American exceptionalism and large-cap US equities and is “risk-on” overall.

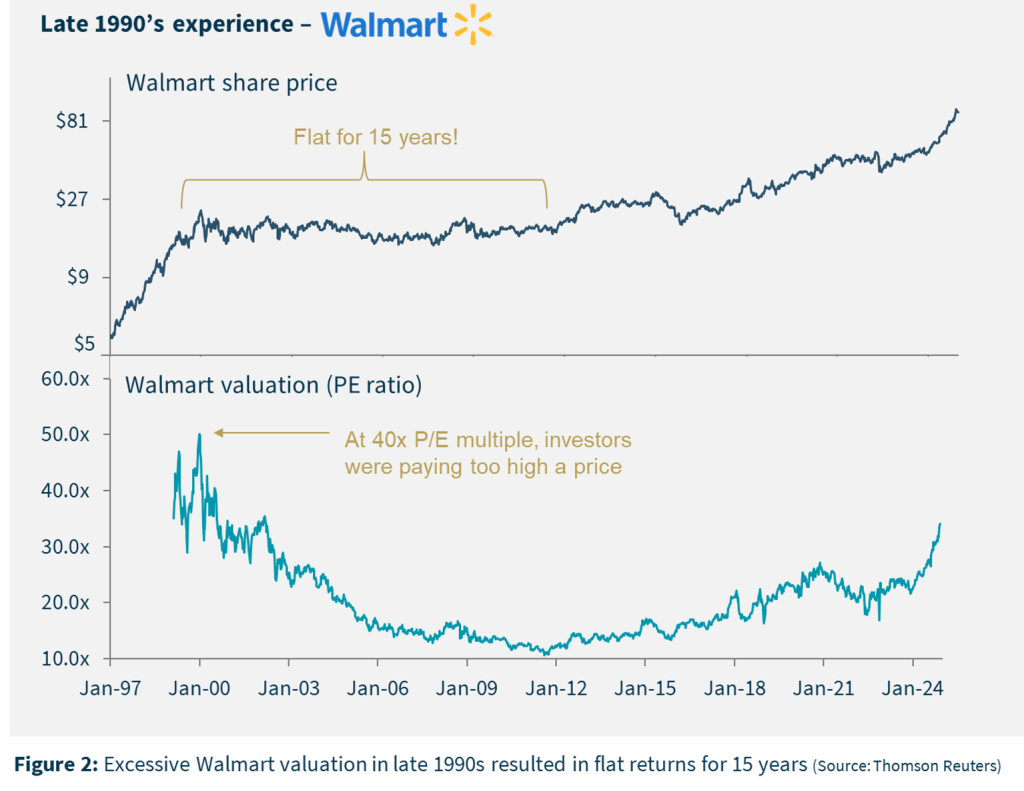

Why does this matter? Because valuations are getting extreme, especially in U.S. public equities, and valuation is a material factor in long-term returns. This is something investors regularly forget in times like this, when a sort of impervious overconfidence takes over. But investing is not only about the asset you buy, but the price you pay for it. A great example of this is Walmart in the 1990s and early 2000s.

Walmart was a retail juggernaut in the 1990s, setting the standard for growth and operational excellence. With its revolutionary supply chain, aggressive pricing strategy, and expansion into Supercenters, Walmart’s dominance was unquestionable. By 1997, it had surpassed $100 billion in annual revenue, marking a decade of phenomenal success. However, despite this impressive performance, its stock entered a prolonged stagnation starting in 1998. For 15 years, Walmart’s stock price moved sideways, even as the company’s revenues and profits continued to climb steadily (see Figure 2).

This disconnect was a function of valuation. Investors in the late 1990s priced Walmart for perfection, pushing its price-to-earnings (PE) ratio to lofty heights. Even as the company delivered consistent business growth, the high expectations baked into its stock price meant there was practically no room for valuation to expand – and plenty of room for it to fall. It wasn’t until Walmart had grown into this valuation and made strategic investments in e-commerce and technology in the 2010s that its stock began to gain momentum again.

The lesson here? No matter how robust the underlying business, paying too high a price can lead to lackluster returns. A business can be great, the economy can be humming, the stock market strong and investor confidence optimistic—and there still needs to be a defensible investment case. One that includes valuation. In fact, it is exactly in times like this, when everything feels exciting and risk has ceded into the dark recesses of the investor mind, when investment case discipline matters most.

“Now is the time to prepare for when the tide does eventually– inevitably –turn.”

Interestingly, Walmart’s valuation is once again approaching 40 times earnings, similar to the late 1990s. And that is despite the company growing at half the rate it did then. Unfortunately, Walmart is but one example of the sort of extreme valuation that characterizes a meaningful part of the S&P500. As the Figure 1 on page 1 suggests, a period of disappointing stock returns may be in store for large parts of the stock market.

Asset class commentary and outlook

Equities

As noted previously, equity markets soared in 2024, driven by a potent mix of economic optimism, monetary easing, American exceptionalism and sectoral outperformance by the so-called Magnificent 7. Technology and large-cap growth stocks led the charge, pushing major indices to levels reminiscent of the late 1990s tech bubble. Valuations have now reached frothy levels in large pockets of the market, with price-to-earnings ratios in certain sectors now significantly above historical averages. Furthermore, the U.S. stock market has become increasingly concentrated, with just 26 stocks now accounting for half of the S&P 500 index’s entire value, a record high level of stock concentration.

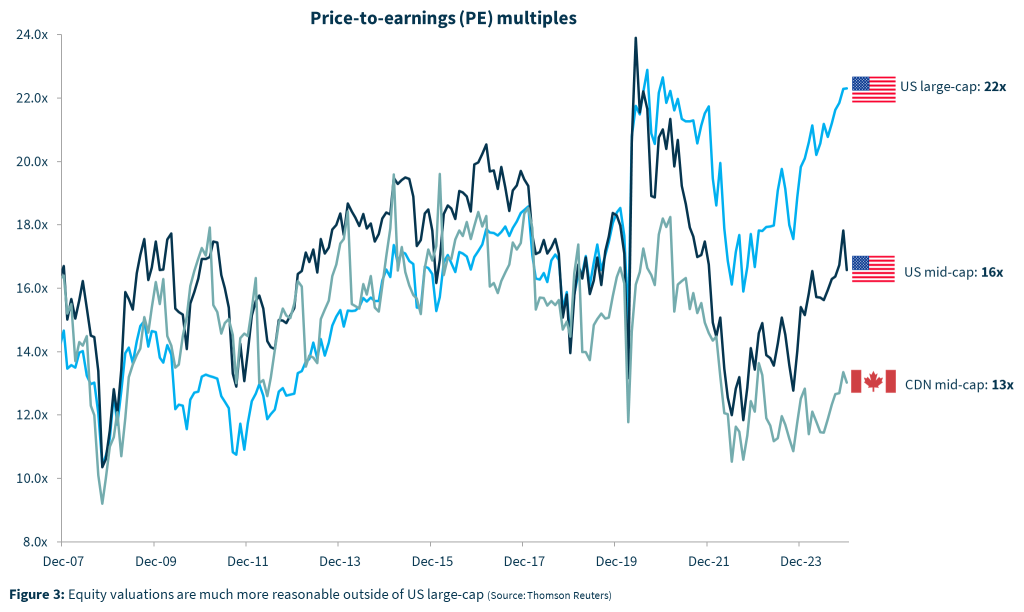

Despite these elevated valuations, opportunities remain in underappreciated segments of the market. Our team finds opportunities in small- and mid-cap stocks in the U.S. and especially Canada, which offer relative value compared to their large-cap counterparts (and a defensible investment case) – especially among those companies that are technically listed on the Canadian stock market but have the majority of their business exposure outside of Canada (see Figure 3). In addition, we find many compelling prospects in higher quality international equities. Currently, the S&P 500’s valuation exceeds that of European stocks by almost 60%, highlighting a significant gap between the two regions. Finally, many of the companies we own also remain attractive potential acquisition targets.

“Looking ahead to 2025, we anticipate continued volatility, driven by inflation, U.S. tariffs, budget deficits, equity valuations, and the potential for sluggish global economic growth.”

In short, the Focus team remains confident and optimistic over the fundamental attractiveness and near and longer-term return prospects of the businesses we own, and skeptical about the broader equity market.

Fixed Income

In 2024, bond markets delivered returns in line with their coupons, reflecting a semblance of normalcy. This period saw both the Federal Reserve and the Bank of Canada initiate a series of interest rate cuts, totaling 1% and 1.75% respectively, in response to moderating inflation and evolving economic conditions. However, this stability belied significant volatility, as yields fluctuated within a broad range throughout the year. Looking ahead to 2025, we anticipate continued volatility, driven by factors such as persistent inflation, the impact of U.S. tariffs, expanding budget deficits, elevated equity valuations, and the potential for sluggish global economic growth.

Interest rates are poised to be a pivotal battleground for financial markets in 2025. Investors mostly appear to expect an easing environment. However, should yields remain elevated, challenges could arise for asset valuations, housing markets, economic growth, and the financing of budget deficits. Inflation will play a crucial role here; it may prove more stubborn than markets currently anticipate, due to tight labor markets, elevated input costs, and the possible repercussions of U.S. tariffs.

An additional question mark is whether 2025 might see the return of “bond vigilantes”. This term refers to investors who sell government bonds (thus driving up yields) in response to fiscal policies they perceive as irresponsible. Currently there are increasing concerns over the new U.S. federal administration’s fiscal policies, including increased government spending and tax cuts, which could lead to higher deficits and inflationary pressures. Should this manifest, we would anticipate it becoming an additional source of market volatility.

Currently within credit, we find more opportunities in low investment grade (BBB) and high-quality issuers of non-investment grade (BB) credit and look for opportunities that are less dependent on market forces (i.e., rates and spreads) that have their own unique catalysts of improvements.

Alternatives

Focus invests in alternatives such as infrastructure, private debt and real estate to provide clients with a much-needed ballast for portfolios and the kind of modern diversification that sophisticated investors like endowment funds have enjoyed for decades. These asset classes offer attractive idiosyncratic return profiles with minimal or no correlation to public markets. Infrastructure and real estate also provide important inflation-hedging characteristics.

In 2024, our alternative investments performed as expected. Within infrastructure, performance was strong in the third quarter 2024 and supported by positive contributions from the investment into AMAROK, a leading provider of contracted perimeter security infrastructure solutions within the United States. AMAROK installs, operates, monitors and maintains solar-powered electric fences and perimeter security solutions on commercial and ongoing structural demand for industrial properties. Within real estate, performance has been supported by the multi-family assets, student housing demand in markets like Montreal, Waterloo, and Kitchener, as well as industrial real estate opportunities in well-located properties with proximity to major distribution centers. Within private debt, borrowers have shown ongoing resilience, driven by increased confidence in the macroeconomic picture.

Looking ahead to 2025 and beyond, it’s important to note that alternatives tend to lag somewhat when the stock market enters periods of aggressive hype. However, it is exactly in periods like now when it is important to build portfolios that can withstand potential turns in the tide. We believe alternatives are poised to play a critical role in mitigating portfolio risk amid potential market volatility.

Final thoughts

Despite the hype and potential volatility, our team at Focus remains confident in the companies in which we are invested and the diversified portfolios we have built for clients. There may be volatility ahead, but we are prepared to use it to our advantage.