The Quarterly Focus – Q3 2024

The following is an excerpt from the quarterly newsletter distributed to clients.

Q3 2024 – Pressure in the plumbing

Global stock markets pulled ahead once again this quarter, though not without experiencing volatility. Central banks continued their delicate balancing act, keeping benchmark rates high enough to combat inflation, yet low enough to support the soft economic landing now widely expected by market participants. Major developed economies, such as the U.S. and Canada, saw continued if more subdued growth, while China introduced a significant reflationary stimulus plan aimed at addressing its debt and structural challenges. Periods of volatility did occur but were short-lived and quickly absorbed by the financial system. Overall, it was another positive quarter for investors.

Yet, signs of fragility within the financial system have emerged. In July, many technology stocks that had previously seen dramatic gains finally corrected. In August, following meetings from the Federal Reserve and the Bank of Japan, investors were convinced that interest rate paths were shifting. As a result, the international carry trade—where funds are borrowed from low-interest currencies and invested into higher-interest ones—began to unwind. The Japanese Yen, typically the borrowing currency, appreciated sharply, while higher-yielding currencies like the Mexican Peso depreciated. Altogether, an estimated ¥40 trillion (roughly $250 billion) was impacted.

Despite these cracks, the financial system remained resilient. If anything, these strains were more reflective of current investor expectations than of, say, deeper, more structural financial system risk.

However, they do point to mounting pressure in the plumbing.

Looking out over current markets, our team finds a little less margin of safety in both equities and fixed income. Investors now largely agree that a “soft landing” and more interest rate cuts are on the horizon, and are, frankly, hypersensitive to any macroeconomic news that questions this consensus. And, with valuations in many pockets of the equity market, especially in the U.S., increasingly priced for perfection, this makes markets generally more susceptible to disappointment. When assets leave little room for error, markets can rapidly become brittle. In the past, we have referenced CNN’s Fear & Greed Index, which mirrors broad sentiment towards the US stock market. As can be seen in Figure 1, investor behavior is currently tilted towards the “greedy” end of the spectrum. The better investment opportunities tend to present themselves when investors are more fearful.

Where does this leave a long-term investor? Ideally, actively investing according to a sound approach. In such an environment, it’s crucial to look for opportunities that are reasonably priced and still afford a margin of safety, while building diversified portfolios that can weather possible inclement weather.

Thankfully, our team continues to uncover attractive investment opportunities that align with this strategy and are positioned to take advantage of and deploy capital into good companies should bouts of volatility occur.

Investment Strategies

Equities

Volatility aside, equity markets performed well during the period in review. The S&P 500 was up 5.89% (4.59% in CAD terms), while the S&P/TSX was up 10.54%. In both Canada and the US, expectations of easing monetary conditions helped boost investor sentiment. In September, the Bank of Canada (BoC) lowered its benchmark interest rate from 4.75% to 4.25%, while the Federal Reserve also cut rates by 50 basis points, lowering its federal funds rate from the 5.25% – 5.50% range to 4.75% – 5.00%. Investors appear to anticipate further cuts in the quarter to come.

“We believe valuations will play a crucial role in shaping market performance going forward”

Looking forward, we believe that businesses with strong cash flows, robust balance sheets, and strategic advantages in their sectors will continue to outperform. While valuations in many pockets of the equity markets remain high, our team continues to find selective opportunities to deploy capital at reasonable valuations, in particular in international markets and North American mid-cap equities. Moreover, several companies in our portfolio remain prime candidates for M&A activity.

We believe valuations will play a crucial role in shaping market performance going forward. At over 29x trailing earnings, the S&P 500 currently trades at historically elevated levels, as do the mega-cap stocks that have dominated equity market performance over the past 18 months. These levels simply do not put the odds in the favour of a long-term investor. Now, as ever, we believe investors must be discerning and maintain some valuation discipline.

Fixed Income

In Q3 2024, fixed income markets in both Canada and the U.S. experienced notable gains, largely due to the favorable shift in monetary policy. The Federal Reserve’s decision to cut rates by 50 basis points, along with a similar move by the Bank of Canada, provided broad support to bonds. Credit also performed well, with the iShares iBoxx High Yield Corporate Bond ETF returning 4.40% in the period.

Looking forward, easing monetary conditions should continue to support fixed income performance. However, whether inflation will be as easily controlled as expected – and therefore the rate of easing as guaranteed — as some assume, remains to be seen.

Moreover, investors should be wary of the current climate of more relaxed credit standards. While high-yield and credit-sensitive sectors have outperformed, there is now increased risk to fixed income investors from, say, a more cavalier treatment of covenants on the part of creditors. This environment makes it especially important to be selective with fixed income investments, and where credit is concerned, picky about quality.

Diversified portfolios and alternative strategies

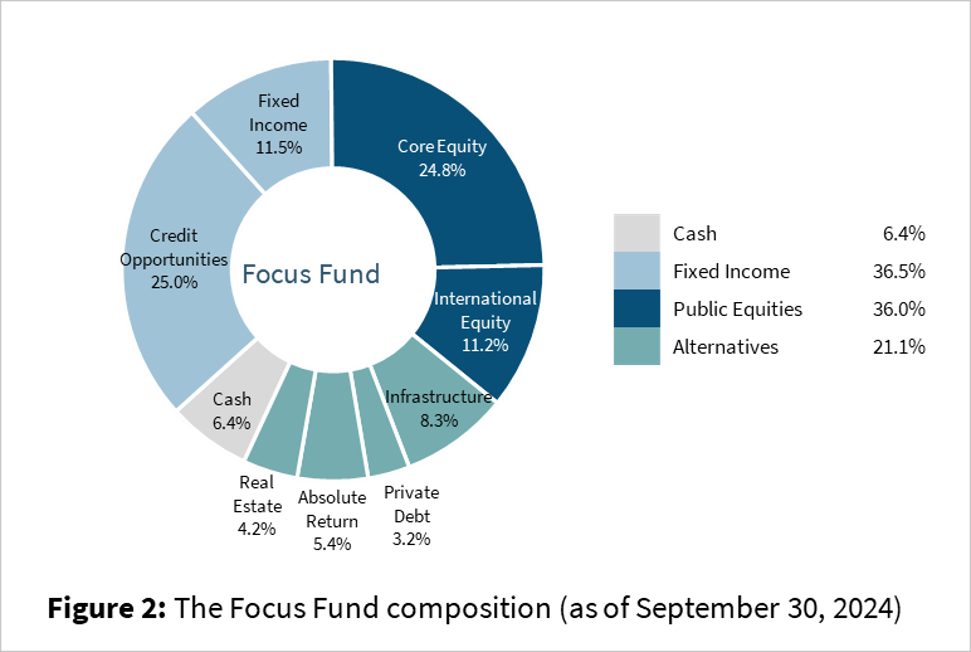

Finally, at 4.62%, the Focus Fund showed solid performance again this quarter. Over the past three years the Focus Fund has delivered an 8.5% annualized return, compared to the 3.5% annualized of the Morningstar Canadian Tactical Balanced Index. This quarter, the Morningstar Canadian Tactical Balanced Index returned 4.9%. See Figure 2 for the asset mix of the Focus Fund as of September.

Our team continues to believe in and advocate for a modern approach to diversification for our clients. This is why our diversified portfolios go beyond a traditional 60-40 mix of stocks and bonds to include real estate, infrastructure, private debt, and absolute return alternative strategies, which offer compelling and uncorrelated risk-adjusted returns. These Focus alternative strategies continue to deliver as expected and perform an important role as ballast in the diversified portfolios.